Journal of Veterinary Medicine And Science

OPEN ACCESS | Volume 3 - Issue 1 - 2026

ISSN No: 3065-7075 | Journal DOI: 10.61148/3065-7075/JVMS

Teklay Asgedom Teferi

Manufacturing Industry Development Institute (MIDI); Leather and leather Products Industry Research and Development Center (LLPIRDC), Addis Ababa, P.O. Box 5, Code 1058, Ethiopia.

*Corresponding author: Teklay Asgedom Teferi, Manufacturing Industry Development Institute (MIDI); Leather and leather Products Industry Research and Development Center (LLPIRDC), Addis Ababa, P.O. Box 5, Code 1058, Ethiopia.

Received: March 10, 2026 | Accepted: April 02, 2026 | Published: April 10, 2026

Citation: Teklay A Teferi, (2026). “Evaluating the Production and Marketing Status of The Ethiopian Leather and Leather Products Sector: - A review of Literature”. Journal of Veterinary Medicine and Science, 3(1); DOI: 10.61148/3065-7075/JVMS/050.

Copyright: © 2026 Teklay Asgedom Teferi. This is an open access article distributed aunder the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

This paper provides a comprehensive evaluation of the current production and marketing landscape of the Ethiopian leather and leather products sector. Historically, the sector has held significant historical significance, being a cornerstone of domestic manufacturing and once contributing a peak share of over 15% to the nation's total export revenue, establishing Ethiopia as a key supplier of high-quality raw hides and skins. The analysis of the current production status reveals a sector with substantial potential, characterized by a vertically integrated industry structure transforming raw materials into finished footwear, garments, and gloves. However, this potential is constrained by inefficiencies in the supply chain and underutilization of installed capacity.

The marketing and export status indicates a strategic shift from exporting semi-processed (crust and wet-blue) leather to higher-value finished leather products (FLPs). Despite this, the export trends show volatility and a failure to reclaim historical export highs, with performance heavily reliant on a few international markets. The sector faces multifaceted challenges, including raw material quality defects, limited access to finance and modern technology, infrastructural bottlenecks, and intense global competition. Conversely, significant opportunities exist in leveraging Ethiopia's abundant livestock population, competitive labor costs, and preferential trade agreements to penetrate niche international markets. The future outlook for the sector hinges on strategic interventions aimed at enhancing product quality, diversifying export markets, and fostering stronger backward and forward linkages. For Ethiopia to realize the full potential of its leather industry, a concerted effort involving policy support, technological upgrading, and strategic marketing is imperative to transition from a supplier of basic commodities to a globally competitive exporter of high-value branded products.

Ethiopian Leather Sector, Production Status, Marketing and Export, Finished Leather Products, Export Trends, Value Addition, Challenges and Opportunities, Future Outlook

The Ethiopian leather and leather products sector holds a significant position both historically and economically within the country. Known for its abundant livestock resources the largest in Africa Ethiopia possesses the capacity to produce over 500 million square feet of finished leather annually, underpinned by a rich heritage in leather manufacturing that dates back more than 80 years (LIDI, 2023; Grumiller et al., 2019). This resource base provides a foundational comparative advantage, positioning the sector as a critical non-agricultural export commodity and a primary source of employment and industrial development (Mekonnen, 2018). The sector has experienced diverse phases, from a historical peak in the 2016/17 fiscal year when export revenues reached USD 140 million to more recent challenges characterized by declining export volumes, quality inconsistencies, and market access difficulties (Tesfaye & Fekadu, 2022; Nuredin, 2011).

The production landscape of the sector reflects a heterogeneous mix of traditional, small-scale artisanal workshops and emerging medium to large-scale tanneries and manufacturing units. These operations are predominantly centered in Addis Ababa and other key regions endowed with high livestock populations, such as Oromia and the Southern Nations, Nationalities, and Peoples' Region (Grumiller et al., 2019; LIDI, 2023). This structure, however, contributes to a critical bottleneck: the fragmentation of the leather value chain. Inefficiencies in the supply of raw hides and skins, often stemming from poor animal husbandry practices, informal market systems, and inadequate preservation techniques at the grassroots level, directly impact the quality and cost of the final product (Gebremariam, 2017; Mulu, 2020). Consequently, despite promising export opportunities to global markets, particularly the European Union, Ethiopian leather exporters face systemic challenges that extend beyond raw material quality. These include persistent capacity underutilization in tanneries, bureaucratic inefficiencies, a lack of cutting-edge technology, and vulnerability to external shocks such as the COVID-19 pandemic and shifts in international trade policy (Tesfaye & Fekadu, 2022; Nuredin, 2011; Wondwossen, 2021).

From a marketing and export perspective, Ethiopia's leather industry is thus poised at a critical juncture between significant potential and profound constraints. Export performance has been volatile, reflecting not only internal production challenges but also fluctuations in global demand and interruptions in regional logistics and stability (Tesfaye & Fekadu, 2022). A key structural issue is the continued reliance on exporting semi-finished (crust and wet-blue) leather, which captures a lower margin compared to high-value finished leather goods like footwear, garments, and leather articles (Gebreyesus, 2015). This limits the sector's export earnings and its integration into higher echelons of the global value chain. The future outlook for the sector, therefore, emphasizes the imperative of strategic interventions. Scholarly and policy consensus points towards the necessity of coherent policy support, targeted technological upgrades, stringent quality control mechanisms, and strategic market positioning to move up the value chain (Grumiller et al., 2019; Ethiopian Leather Industry Development Institute, 2016). Success in these areas is deemed crucial for Ethiopia to regain its competitive edge and sustainably expand its share within the dynamic global leather market.

The objective of this paper is:-

1. Production Status

a. Raw Material Availability: Ethiopia possesses a vast livestock population, including approximately 70.3 million cattle, 42.9 million sheep, and 52.5 million goats. This abundance of hides and skins provides a solid foundation for the leather industry, with an estimated 8-10 million cattle hides and 15-18 million skins (sheep and goat) available annually (CSA, 2021).

b. Tanning and Manufacturing: The sector is composed of both large-scale, private-owned tanneries and a significant number of small-scale enterprises. There are around 34 tanneries in Ethiopia, with a mix of local and foreign direct investment (FDI) ownership (Mekonnen et al., 2021). These tanneries are the main suppliers of finished leather to local manufacturers and also contribute a large share of the country's leather exports (Gebreeyesus & Iizuka, 2012). The manufacturing segment includes shoe factories, glove factories, and producers of leather goods and garments (UNIDO, 2017). The shoe industry, in particular, is a growing sector, producing millions of pairs for both local consumption and export (Lall & Mengistae, 2011).

c. Traditional Production: Traditional leather processing and production also play a vital role, especially in rural communities. Traditional tanners are responsible for a large volume of raw cattle hides being processed into household goods and other products. However, these traditional methods often face challenges such as environmental pollution and a lack of modern techniques (Teka, et al., 2016).

2. Marketing and Export Status

A. Export Performance: The Ethiopian leather sector has seen growth in its export earnings, though it has faced fluctuations. In 2019/2020, the country exported over $135 million worth of leather and leather products (DART Consulting, 2023). However, there has been a recent decline in export earnings, with a 9.1% drop in 2021/22, accounting for about $32 million in earnings (Shemsu, 2024).

B. Export Destinations and Products: The primary destinations for its exports are concentrated in key global markets. According to a sector analysis by the World Bank, China, Italy and Hong Kong are the major importers of Ethiopian leather and leather products (World Bank, 2020, p. 25). Traditionally, the sector's exports have been dominated by semi-processed or finished leather, with sheep and goat skins being particularly notable for their quality (OEC, 2022). However, recognizing the limitations of relying on raw material exports, the Ethiopian government and industry stakeholders have been actively pursuing a strategic shift. This strategy explicitly aims to move up the value chain by promoting the manufacture and export of value-added products, such as footwear, gloves, bags, and other leather goods, to capture higher profits and increase foreign exchange earnings (UNIDO, 2017, p. 12; World Bank, 2020, p. 30).

C. Domestic Market: The domestic market for leather products is significant but faces intense competition from cheaper imported goods, including synthetic alternatives (World Bank, 2020). In response, government-led initiatives like 'Ethiopia Tamirt' aim to promote locally made products and bolster domestic consumption to support small and medium-sized enterprises (SMEs) (World Bank, 2020). Ethiopian SMEs in the leather sector contend with a domestic market flooded with competitive imported goods (Gebreeyesus, 2018). Initiatives such as 'Ethiopia Tamirt' are examples of the government's efforts to create a protective market space for these local enterprises by encouraging domestic consumption (Gebreeyesus, 2018). The 'Ethiopia Tamirt' movement is a central government-led initiative designed to foster a culture of purchasing locally made goods, thereby strengthening the domestic market for SMEs against international competition (EEA, 2021).

3. Challenges and Opportunities

a. Challenges:

Raw Material Quality: The challenge of raw material quality, stemming from inadequate husbandry, slaughtering, and preservation practices, is a well-documented and critical bottleneck in the leather production value chain, particularly in developing nations like Ethiopia.

A primary challenge originates at the animal husbandry stage. Inadequate practices, such as communal grazing on rough pastures and a lack of veterinary care, lead to a high incidence of skin defects like tick bites, branding marks, and scars. As noted by Mekonnen et al. (2020), these pre-slaughter defects significantly downgrade the quality and value of hides, making them unsuitable for high-value leather goods. The problem is often exacerbated by poor animal health management, which directly correlates to the density and severity of defects on the raw material.

Furthermore, the methods used during slaughtering and the immediate post-slaughter phase introduce critical flaws. Traditional or unregulated slaughtering techniques, often involving deep knife cuts, contribute to flay marks and scores that irreparably damage the grain layer the most valuable part of the hide. Ahmad et al. (2019) emphasize that flaying defects are a major cause of quality depreciation, directly reducing the area of usable leather and, consequently, the economic return. The lack of standardized training for butchers and flayers is a key factor perpetuating this issue.

Finally, improper preservation methods after flaying severely degrade the raw material before it even reaches the tannery. In many regions, sun-drying or curing with excessive salt remains common practice. Sun-drying causes irreversible fiber collapse and brittleness, while uneven salting leads putrefaction and bacterial damage. Bekele et al. (2021) found that a significant percentage of hides and skins are downgraded at the tannery level due to spoilage caused by ineffective preservation during storage and transportation. This degradation directly "impacts competitiveness in the international market," as tanneries cannot produce consistent, high-quality leather from compromised raw materials, forcing them to compete on price rather than quality in the global arena (Gebrehiwot, 2022).

Technological and Skill Gaps: Many tanneries and factories use outdated equipment and techniques, resulting in low-quality final products. A lack of skilled labor and limited training programs further exacerbates this issue (allAfrica.com, 2024).

Environmental Concerns: The traditional and some modern tanning processes involve harmful chemicals, leading to significant environmental pollution of water bodies and air. The high cost of waste treatment is a major challenge for businesses (allAfrica.com, 2024; UNIDO, 2023).

Market Linkages and Policy Gaps: Poor market linkages, which increase transaction costs for smallholder farmers (Key et al., 2000), and a high involvement of middlemen, who often arise to fill institutional voids but can lead to exploitative interlocked contracts (Bardhan, 1980; Fafchamps, 2004), constrain agricultural development. Furthermore, inadequate access to foreign currency for importing essential inputs like chemicals reflects a critical macroeconomic policy gap. This shortage can be understood through the lens of the "foreign exchange gap" (Chenery & Strout, 1966) and is often exacerbated by exchange control regimes that distort incentives and cripple productive sectors (Bhagwati, 1978).

b. Opportunities:

Abundant Raw Materials: The vast livestock population of Ethiopia remains the single most important advantage for the leather industry, providing a foundational competitive edge. Ethiopia possesses one of the largest livestock populations in Africa and the world, (CSA, 2017, as cited in Gheze et al., 2021). This immense resource provides a critical mass of hides and skins, which are the primary raw materials for leather production. The domestic availability of these materials reduces reliance on expensive imports, thereby lowering input costs and providing a natural buffer against global supply chain disruptions (Mekonnen et al., 2020).

The quality and type of the raw materials also present a significant opportunity. Ethiopian sheepskins, in particular, are internationally renowned for their unique hair pattern, softness, and suitability for high-value products like luxury gloves, footwear uppers, and fashionable garments (Gebremariam et al., 2016). This inherent quality allows Ethiopian tanneries to target premium market segments rather than competing solely on price in the bulk leather market. Furthermore, the predominance of cattle hides supports the production of a wide range of goods, from sturdy footwear soles to upholstery leather, enabling product diversification within the sector (Mulugeta, 2018).

However, it is crucial to note that the mere abundance of raw materials does not automatically translate into a competitive industry. The full potential of this opportunity is contingent upon addressing critical challenges in the upstream supply chain. As noted by Gheze et al. (2021), the high prevalence of pre-slaughter and post-slaughter defects, such as branding marks, scratches, and poor flaying techniques, significantly downgrades the quality and value of hides and skins. Therefore, while the resource base is a powerful inherent advantage, its effective utilization requires parallel investments in animal husbandry, hide and skin collection systems, and immediate preservation practices to prevent spoilage and maximize economic return (Mekonnen et al., 2020).

Government Support: The Ethiopian government has recognized the potential of the sector and has implemented initiatives to promote it. This includes the establishment of the Ethiopian Leather Industry Development Institute (LIDI) to provide sector-specific support (Gebremeskel & Mebratu, 2020), the creation of specialized industrial parks like Modjo Leather City to foster clustering (Oqubay & Tesfachew, 2019), and the implementation of policies specifically designed to encourage value addition over raw material export (UNIDO, 2015).

Market Access: Ethiopia's duty-free access to major markets like the European Union (under the Everything But Arms initiative) and the opportunities presented by the African Continental Free Trade Area (AfCFTA) offer significant potential for export growth. This potential is grounded in trade theories that highlight how preferential market access can catalyze export diversification in developing countries (Baldwin, 2016). Empirical studies on the EBA initiative have shown its role in boosting exports from Least Developed Countries (Gamberoni, 2007); while economic models project that the AfCFTA could substantially increase intra-African trade and export-led industrialization (UNECA & African Union, 2020).

Investment and Collaboration: Investment and Collaboration: The sector is attracting both domestic and foreign investment, a phenomenon well-explained by frameworks analyzing the location-specific advantages that attract multinational enterprises (Dunning & Lundan, 2008). Furthermore, there is a growing focus on developing supporting industries; a strategy long advocated creating strong backward linkages within an economy (Hirschman, 1958). This is coupled with the promotion of industrial clusters, which are recognized as a key source of productivity and competitive advantage (Porter, 1998). Together, these strategies are central to a nation's effort to upgrade its position within global value chains by enhancing local capabilities and systemic efficiency (Gereffi et al., 2005).

Export Trends of the Ethiopian Leather and Leather Products

Trends in Export Performance

As part of its state-led development strategy, the Ethiopian government has actively sought to transform the leather sector from exporting raw hides and skins to higher-value finished products like footwear and garments (Oqubay, 2015). This policy, involving export bans on raw materials and investment in industrial clusters, aimed to capture greater value and create manufacturing jobs. However, studies indicate that the transition to complex finished goods has faced significant challenges related to technological capabilities and learning within local firms (Whitfield et al., 2020).

Shift from Raw Materials to Finished Products: A central trend in the Ethiopian leather industry has been a strategic policy-driven shift from exporting raw and semi-processed materials to focusing on value-added finished goods. To catalyze this transition, the Ethiopian government implemented a decisive fiscal measure in 2008, imposing a 150% export tax on semi-processed "wet-blue" leather (Fitawek et al., 2019). This policy was designed explicitly to disincentivize the export of intermediate goods and foster domestic value addition, a goal that aligns with the broader industrial development strategies observed in other developing nations (Oqubay, 2015). The policy framework was further reinforced in 2012 by extending the export tax to include the more processed crust leather, thereby deepening the incentive structure for local manufacturers to engage in final production stages (Fitawek & Kalaba, 2016).

The direct impact of these policies is evident in the subsequent export composition data. As documented by Fitawek et al. (2017) and supported by the broader analysis of Gebreeyesus (2016) on industrial policy, the export volumes of semi-finished leather experienced a marked decline following these interventions. Concurrently, exports of finished leather products, particularly footwear, registered a significant increase (Fitawek et al., 2017). This trend underscores the influence of targeted industrial policy in reshaping a nation's export profile and moving up the global value chain, a transition also observed in other developing economies pursuing similar export-oriented industrialization strategies (Whitfield et al., 2020).

Growth in Finished Leather and Footwear Exports: The strategic policy shift in Ethiopia's leather sector, particularly the export tax on semi-processed hides and skins, successfully incentivized the export of higher-value goods. This policy intervention led to a notable growth in the export of finished products. For example, between 2007 and 2013, the export of finished leather and footwear increased by 75% and 44%, respectively (Fitawek & Kalaba, 2016). A significant driver of this growth has been foreign direct investment (FDI), with Chinese companies playing a prominent role. As noted in subsequent research, many of these foreign firms have established export-oriented production facilities, focusing heavily on manufacturing footwear destined for international markets like the USA, often leveraging preferential trade agreements (Gebremeskel et al., 2020).

Export Destinations: A dominant trend in recent decades has been the increasing importance of China as the primary export destination for Ethiopian leather. Research indicates that this relationship is largely driven by China's demand for raw and semi-processed materials. As noted in a study on the sector's competitiveness, "China has become the main destination for Ethiopian semi-processed leather (e.g., wet-blue and crust leather), absorbing a significant share of the country's exports" (Gebreeyesus & Iizuka, 2012, p. 18). This shift signifies a move away from higher-value finished products towards intermediate goods, which fetch lower prices on the global market.

Traditionally, European countries, particularly Italy, have been the cornerstone of Ethiopia's high-value leather exports. Italy, with its renowned leatherworking and fashion industry, has been a key market for higher-quality finished leather and products. However, competition and challenges in meeting stringent quality standards have impacted this trade. As one analysis points out, while Italy remains a critical destination, its share has been challenged by "the inability of Ethiopian tanneries to consistently meet the quality and environmental standards required by the high-end Italian market" (Mekonnen et al., 2017, p. 45). This has reinforced the pivot towards less demanding markets for semi-processed goods.

The concentration on a limited number of export destinations like China and Italy presents both a pattern and vulnerability. A study on the export performance of the leather industry highlighted that "the heavy reliance on a few markets, specifically China for semi-processed leather and Italy for some finished leather, makes the sector highly susceptible to external demand shocks and changes in international trade policies" (Gebreeyesus, 2016, p. 112). This lack of market diversification is consistently identified as a critical risk factor for the long-term stability and growth of Ethiopia's leather export earnings.

Challenges and Constraints

Challenges,

The leather and leather products sector faces several structural challenges that continue to hinder its full potential and export competitiveness.

Quality of Raw Materials: A primary and persistent challenge constraining the growth of the Ethiopian leather industry is the inferior quality of its raw hides and skins. This problem is multifaceted, originating from pre-slaughter to post-slaughter stages. As Gebremichael et al. (2023) detail, poor animal husbandry practices, including widespread parasitic diseases, branding marks, and poor nutrition, directly damage the hide and skin, reducing its value and suitability for high-end products (p. 45).

The challenges continue after the animal's life. Inadequate flaying (skin removal) techniques at slaughterhouses, often using sharp tools that cause deep scores and scratches, further degrade the material. This is compounded by insufficient and unhygienic preservation methods. A significant study by Mekonnen et al. (2022) found that the predominant use of sun-drying and salt-curing with contaminated salt leads to putrefaction, hair slip, and a brittle final product. Consequently, as their research quantifies, "only about 15-20% of the national raw material collection meets the quality standards required for producing export-oriented finished leather goods" (p. 112). These low-grade input forces tanneries to either produce lower-value items or incur high costs to rectify defects, severely undermining the sector's international competitiveness.

Supply Chain Bottlenecks: The primary supply chain bottleneck in the Ethiopian leather industry lies in the severe disconnect between the country's vast livestock population and the quantity and quality of raw materials that ultimately reach tanneries. As noted, a significant portion of the raw material goes uncollected or is lost due to damage and spoilage before it can be processed. This inefficiency begins at the source, where traditional animal husbandry practices and widespread subsistence farming lead to a highly fragmented supply of raw hides and skins, characterized by poor quality due to diseases, branding wounds, and other pre-slaughter defects (Gebremichael & Gopal, 2021). Furthermore, the lack of a coordinated collection system and inadequate preservation methods at the abattoir and collection point levels result in substantial post-mortem losses. A study by Mulugeta (2019) estimated that up to 30% of potential hide and skin production is lost annually due to putrefaction and poor handling, severely constraining the raw material pipeline for tanneries and undermining the sector's export potential.

1. Inefficient Collection and Poor Preservation Systems

A major issue is the lack of a well-organized and widespread collection system. The majority of animals are slaughtered in rural areas or by informal butchers, where there is little knowledge or incentive for proper flaying and initial preservation. The traditional practice of defective flaying using knives to make incisions that damage the hide is a primary cause of quality degradation (Mekonnen, 2020). This results in scars, cuts, and brand marks that drastically reduce the value of the leather.

Furthermore, the absence of immediate and proper preservation at the source is catastrophic. As noted in a sector analysis, "the lack of adequate preservation facilities and the use of traditional methods like sun-drying or salting with contaminated salt lead to putrefaction, hair slip, and other defects" (Gebremariam & Tesfaye, 2021, p. 45). This poor upstream handling means that a large quantity of hides and skins that do enter the supply chain are already of sub-standard quality before they even reach the first intermediary.

2. Proliferation of Intermediaries and Market Inefficiency

The journey of a hide from a rural slaughterhouse to a tannery is typically characterized by a long chain of multiple intermediaries. This fragmented structure has two direct negative consequences: inflated costs and compromised quality. As Mekonnen (2020) explains, "the existence of numerous intermediaries in the supply chain increases the final price of raw hides and skins for tanneries without adding any value to the product" (p. 108). Each intermediary seeks a profit, driving up the input cost for tanneries and making them less competitive internationally.

Moreover, this extended chain increases the time between flaying and processing, exacerbating preservation problems. The lack of a formal and transparent market mechanism means that tanneries have little direct control over their most critical input. A recent study on supply chain governance concluded that "the weak vertical coordination between tanneries and their raw material suppliers is a fundamental constraint to improving quality and ensuring a consistent supply" (Gebreslassie, 2022, p. 12).

Other Critical Constraints in the Sector

While the raw material supply chain is a foundational bottleneck, it is compounded by other significant challenges.

1. Limited Value Addition and Product Diversification

The sector has historically been geared towards the export of semi-processed (crust and wet-blue) leather rather than finished products. This limits the value captured within Ethiopia. Although there is a policy push towards exporting finished goods, the capability is still limited. MoI (2019) reported that "the capacity to produce high-value, finished leather products such as footwear, garments, and leather goods is constrained by technological gaps, design limitations, and a lack of skilled manpower" (as cited in Gebremariam & Tesfaye, 2021, p. 47).

2. Inadequate Environmental Compliance and Technological Gaps

Tanneries are faced with the global challenge of adhering to stringent environmental regulations. Effluent treatment is a significant cost and operational hurdle. Many tanneries struggle with outdated machinery and inefficient production processes, which not only affect productivity but also make compliance with international environmental and chemical safety standards (e.g., REACH) difficult (Mekonnen, 2020).

3. Policy Instability and Inconsistent Incentives

Frequent changes in export policy, such as shifting bans and incentives on semi-processed versus finished leather, create an unpredictable business environment for investors. This discourages long-term investment in the sophisticated machinery and training required for high-end manufacturing.

Limited Technological and Design Capability: The Ethiopian leather sector faces significant challenges due to limited technological and design capabilities. A primary constraint is the widespread lack of modern machinery and a shortage of skilled labor proficient in contemporary leather technology and innovative design (Moges et al., 2021). This technological and skill gap severely restricts the sector's capacity to meet the stringent demands of the high-end global market, which requires sophisticated, fast-changing designs and a diverse product range (ALLPI, 2023). Consequently, Ethiopian firms are often unable to move beyond the production of basic commodity leather and simple manufactured goods, hindering their international competitiveness and value addition (Gebremariam, 2020).

Environmental and Infrastructure Issues: The Ethiopian leather sector faces significant environmental and infrastructure challenges that constrain its development. The tanning process is a primary concern, as it generates substantial waste and pollutants, and the widespread lack of adequate industrial waste treatment facilities exacerbates its environmental impact (Mekonnen et al., 2021). Furthermore, the absence of robust local supporting industries, particularly for tanning chemicals, forces manufacturers to rely on imported inputs. This dependency increases production costs and renders the sector highly vulnerable to global supply chain disruptions and foreign exchange fluctuations (UNIDO, 2018).

Opportunities and Future Outlook

Despite the challenges, the Ethiopian leather and leather products (LLP) sector holds considerable potential for growth, largely driven by strategic government initiatives. The government has explicitly identified the LLP sector as a priority for industrial development, aiming to capitalize on the country's large livestock population the largest in Africa as a source of raw materials (Gebremeskel, 2020).

Industrial Parks: The cornerstone of this strategy is the development of specialized industrial parks. The establishment of the Modjo Leather City, along with other leather-focused clusters in larger parks like Hawassa and Bole Lemi, is a key government initiative designed to create a more conducive environment for both foreign and local investors. As noted in a recent United Nations Industrial Development Organization (UNIDO) report, these parks provide critical infrastructure and shared facilities, which are essential for modern and efficient manufacturing (UNIDO, 2023). A significant feature of these parks, as highlighted by UNIDO (2023), is the inclusion of a Common Effluent Treatment Plant (CETP), which directly addresses the serious environmental concerns associated with tannery operations by providing a centralized waste water treatment solution. This model of clustered development is seen as vital for enhancing productivity, fostering innovation, and improving the sector's international competitiveness (Mekonnen et al., 2021). By concentrating production and providing essential services, these parks are poised to help Ethiopia move up the value chain from exporting raw hides and semi-finished leather to producing high-value finished leather goods for export markets.

Regional Integration: Regional integration, particularly through the African Continental Free Trade Area (AfCFTA), presents a transformative opportunity for the Ethiopian leather industry. The agreement establishes a single market for goods and services, offering Ethiopian producers preferential access to a vast and growing market of over 1.4 billion people across the continent (UNECA, 2023). This market access is critical for diversifying export destinations and reducing the sector's historical dependency on a limited number of traditional markets, which has often constrained its bargaining power and growth potential (Gebreeyesus, 2016). By leveraging the AfCFTA's provisions to reduce tariff and non-tariff barriers, the sector can achieve economies of scale, enhance its competitiveness, and move up the value chain from exporting raw hides and semi-processed leather to finished consumer goods (Melesse, 2021). This strategic shift is seen as essential for capturing greater value and ensuring the long-term sustainability of the industry.

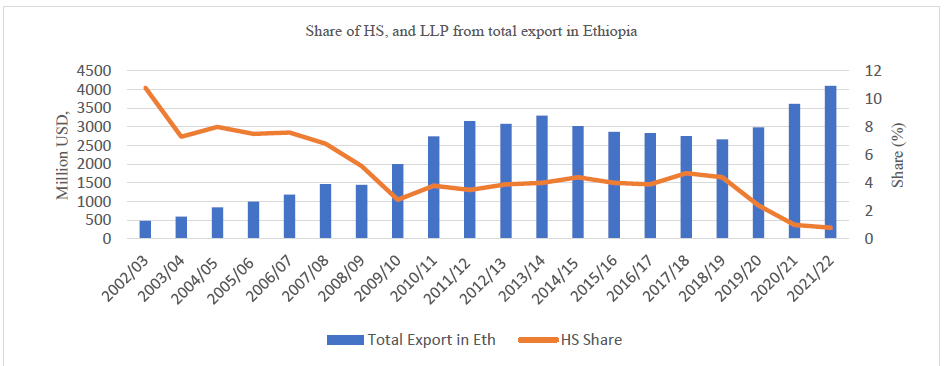

Share of Leather and Leather Products export from Ethiopian commodity

The leather and leather products sector has historically been one of the top five export commodities of Ethiopia, alongside coffee, gold, chat, and oilseeds. However, its relative share has experienced a significant decline over the past two decades. While it once consistently held a share of over 10% of national export earnings, its contribution has fluctuated and generally trended downwards, often falling to between 2% and 4% in recent years (Gebreeyesus, 2016; Mulu, 2020). This decline is attributed to a combination of internal challenges and external market factors. Internally, the sector has been hampered by issues such as inconsistent raw material quality and policy instability, which have hindered competitiveness and investment (Mekonnen et al., 2017; Zewdie & Oljira, 2021). Externally, fluctuating global demand and stringent international quality and environmental standards have presented significant obstacles (Gebreeyesus, 2016).

Figure 1: Share of HS, an LLP export from Ethiopian total export; Source: NBE. (Rehima M., 2025)

1. Historical Significance and Peak Share

The leather industry is one of Ethiopia's oldest manufacturing sectors. Due to the country's large livestock population (the largest in Africa), the sector has a strong natural resource base. During the 1990s and early 2000s, it was a major source of foreign currency (Oqubay, 2015).

Historical Significance of the Ethiopian Leather Sector

The historical significance of the Ethiopian leather sector is deeply rooted in the country's agrarian economy and artisanal traditions. For centuries, leatherworking was a well-established craft, producing items essential for daily life, such as footwear, bags, harnesses, and parchment, using indigenous knowledge and techniques. This pre-industrial craft was not merely an economic activity but was embedded in the social and cultural fabric, with specific communities, such as the tanning caste, specializing in the labor-intensive and ritually "unclean" process of skin preparation (Pankhurst, 1968). The products of this era, including shields, manuscripts, and traditional attire, were vital to the functioning of the highland Ethiopian state and society (Abir, 1968).

The sector's transition to modern industrial significance began under Emperor Haile Selassie's reign (1930-1974), as part of a broader state-led strategy for economic modernization. The government identified leather as a key non-agricultural export commodity capable of generating foreign exchange. This period saw the establishment of the first modern tanneries, which were capital-intensive, state-owned, or state-supported enterprises designed to shift from exporting raw hides and skins to exporting semi-finished and finished leather goods (Lange, 2017). This industrial policy was a deliberate move to capture more value from the country's vast livestock resources, which is one of the largest in Africa.

The Djibouti-Addis Ababa railway, completed in 1917, was a critical precursor to this industrialization, as it facilitated the export of hides and skins to international markets, thereby integrating the Ethiopian raw material base into the global economy (Pankhurst, 1968). The modern tanneries established in the post-World War II era were heavily reliant on foreign expertise and technology, particularly from Italy and India, marking a significant technological shift from indigenous tanning methods (Fischer, 2021). This state-led industrial drive cemented the leather sector's role as a cornerstone of Ethiopia's modern manufacturing base, a status it has retained, though with varying degrees of success, through subsequent political regimes, including the Derg and the current EPRDF-turned-Prosperity Party governments (Oqubay, 2015).

As Gebreeyesus and Sonobe (2012) detail, "the modern leather and leather products industry in Ethiopia dates back to the imperial regime in the 1920s," with the establishment of the first modern tannery in Addis Ababa in 1929 (p. 2). This marked the formal transition from a purely artisanal craft to an organized industrial sector aimed at import substitution and, later, exports. The sector's strategic importance was further cemented during the Derg regime (1974-1991), which nationalized most large-scale tanneries and integrated the industry into its state-controlled, centrally planned economy. The primary focus was on exporting semi-processed (crust and wet-blue) leather to earn vital foreign exchange. As noted by Lall (1999), developing countries often rely on resource-based exports as an initial stage of industrial development, and Ethiopia's leather sector was a classic example, leveraging the country's large livestock population the largest in Africa as its primary raw material base (p. 12). This period solidified the leather industry's role as one of the "traditional three" pillars of Ethiopian manufacturing, alongside textiles and food processing.

Peak Market Share

Based on available historical analyses, determining a precise "peak market share" for the Ethiopian leather sector on a global scale is challenging due to a lack of consistent international data. However, both academic and industry sources concur that the sector's highest level of international prominence and contribution to the national economy was achieved in the late 1960s and early 1970s, just prior to the political upheavals of the Derg regime (Gebreeyesus & Sonobe, 2012; Lall, 1999). During this peak period, leather and leather products constituted a dominant source of Ethiopia's export revenue, establishing the industry as a cornerstone of the nation's early manufacturing exports. As Gebreeyesus and Sonobe (2012) state, "the leather industry was one of the country’s major manufacturing export earners during the 1960s and 1970s" (p. 2). While a specific global market share percentage is elusive in the literature, the sector's dominance within the national export context is unequivocal. It accounted for a significant portion of Ethiopia's non-agricultural exports, with one of its most critical markets being the Italian luxury goods industry, which highly valued the exceptional quality of Ethiopian sheepskins in particular (Gebreeyesus, 2009; Lall, 1999).

This peak was not sustained. The nationalization and central planning of the Derg era, coupled with a lack of investment and technological upgrading, led to a gradual decline in the sector's global competitiveness. As Oqubay (2015) argues in "Made in Africa: Industrial Policy in Ethiopia," the sector struggled for decades with inefficiencies and a focus on low-value-added semi-processed goods, preventing it from reclaiming its former stature in the global market (p. 178). The peak market share was thus a reflection of a specific historical moment when Ethiopia had a comparative advantage in raw and semi-processed leather, before other global producers advanced and the Ethiopian industry failed to keep pace.

In the modern era, despite concerted government efforts to promote leather product exports, particularly footwear, through industrial policies and the establishment of specialized industrial parks, the sector's global market share remains a fraction of what it was at its historical peak (Gebreeyesus, 2016; Oqubay, 2018). This decline in global standing persists even as the leather and footwear industry continues to be strategically targeted by the Ethiopian government for its job creation potential and its role in the broader industrialization agenda (Lall & Mengistae, 2005; Oqubay, 2015).

In the early 2000s, the leather and leather products sector was identified as a pivotal priority within Ethiopia's Industrial Development Strategy (IDS) (Oqubay, 2015). The government's ambitious roadmap aimed to dramatically increase the sector's export value from US$32 million in 2003/04 to US$500 million by 2014/15 (Oqubay, 2015). During its peak influence in national policy discussions, the sector's share of total merchandise exports was significant, underscoring its perceived role as a leading vector for industrial transformation (Gebreeyesus, 2013). However, this prominence began to wane as the sector faced stiff competition from other emerging export sectors, most notably horticulture, which started to capture a growing share of Ethiopia's non-traditional exports (Lavers, 2021).

World Bank (2012) report highlights that in the fiscal year 2009/10, leather and leather products accounted for about 6% of Ethiopia's total export earnings. This was a period when the sector was still considered a cornerstone of the country's export-oriented industrialization strategy, a policy position extensively analyzed in the academic literature (Oqubay, 2015). The performance of the leather sector during this time was seen as a critical test case for Ethiopia's state-led industrial policy (Whitfield & Staritz, 2021).

2. Recent Trends and Declining Market Share of the Ethiopian Leather Sector (2010s – Present)

The Ethiopian leather industry, once a flagship sector for the country's industrialization ambitions, has faced a significant downturn from the 2010s to the present. Despite possessing one of the largest livestock populations in Africa and a rich raw material base, the sector has struggled to translate this potential into global market success, resulting in a declining market share. This decline is the result of a complex interplay of internal constraints and shifting external market dynamics.

1. Policy Shifts and the Export Ban on Raw Hides and Wet-Blue

The Ethiopian government's policy shifts in the leather sector during the 2010s involved a prominent ban on exporting raw hides and wet-blue (semi-processed) leather, intensified in 2010 and again in 2018. This export ban aimed to incentivize domestic value addition by boosting finished leather and leather product exports, thus capturing more value within the national supply chain (Gebreeyesus, 2016). The government also imposed hefty export taxes up to 150% in some cases on raw hides and wet-blue to discourage exports without value addition, with the intention to stimulate local tanning and manufacturing capacity (Oqubay, 2015).

However, the policy led to unintended consequences. The domestic tanning industry faced serious challenges due to outdated technology, inefficient resource use, and high production costs, which undermined its competitiveness in producing high-quality finished leather demanded by international markets. Consequently, the sector became trapped between the inability to export raw materials and the failure to offer competitive finished products, which severely limited market growth and international presence. As Oqubay (2015) emphasized, industrial policy should be grounded in firm-level capabilities and global market dynamics, which this policy failed to account for effectively. Many tanneries operated under capacity or closed down due to lack of working capital, quality supply issues, and environmental regulations, reflecting the domestic industry's low competitiveness (Gebreeyesus, 2016; Brautigam et al., 2018). In summary, while the export ban on raw hides and wet-blue sought to promote domestic value addition and increase finished leather exports, the underdeveloped state of Ethiopia’s tanning industry created a bottleneck that reduced export volumes and market share, illustrating the gap between policy aims and industrial capabilities (Gebreeyesus, 2016; Oqubay, 2015; Brautigam et al., 2018).

2. Declining Competitiveness and Quality Issues

A primary driver of the sector's declining market share has been its eroding competitiveness. Ethiopian leather products have consistently faced challenges related to quality, price, and compliance with international standards. A key issue is the poor quality of raw hides due to widespread pre-slaughter and post-slaughter defects. Lemma et al. (2021) highlight a United Nations Industrial Development Organization (UNIDO, 2017) report, noting that branding, scratches, and tick marks are estimated to affect over 60% of the national hide supply. This fundamental input problem results in a low yield of high-quality finished leather.

Furthermore, domestic tanneries and manufacturers have been slow to adopt modern technology and best practices. Compared to competitors in Asia, Ethiopian firms suffer from higher production costs, driven by unreliable infrastructure, expensive financing, and bureaucratic hurdles (Lemma et al., 2021). This has prevented the industry from moving into higher-value market segments. Analyzing the leather industry's global value chain, Whitfield and Staritz (2021) found that "Ethiopian firms are largely relegated to the lower-value, more volatile segments of the market, struggling to meet the stringent quality and delivery schedule requirements of lead firms in Europe and North America" (p. 215). This inability to integrate reliably into global value chains has directly contributed to the loss of market share.

3. The Rise of Asian Competition and Shifting Global Demand

While Ethiopia grappled with internal challenges, global competition intensified dramatically. Asian manufacturers, leveraging formidable economies of scale, advanced technological adoption, and highly developed supply chain ecosystems, captured an increasing share of the global leather goods market (Gereffi & Frederick, 2019). This regional dominance is not merely a function of cost but of deeply integrated production networks that efficiently transform raw materials into finished goods for export. Vietnam, for instance, solidified its position as a major exporter of footwear to the EU, a trajectory accelerated by preferential trade agreements like the EU-Vietnam Free Trade Agreement (EVFTA) and significant inflows of foreign direct investment that modernized its production capabilities (Nguyen & Hens, 2023). This strategic positioning allowed countries like Vietnam to move beyond basic assembly to more complex, value-added manufacturing, directly competing in the same markets that Ethiopian producers aimed to enter (World Bank, 2020).

The nature of global demand also shifted towards faster fashion cycles, smaller order quantities, and more complex design requirements that the relatively inflexible Ethiopian industry struggled to meet. This shift in global value chain (GVC) governance, driven by lead firms in the Global North, placed a premium on supplier capabilities beyond low cost, a trend extensively documented in the literature (Gereffi, Humphrey, & Sturgeon, 2005). The competitive advantage of Asian producers became "not just about cost, but about speed, flexibility, and the ability to service large, sophisticated buyers" (Gereffi & Frederick, 2019, p. 20). This was underpinned by their development of full-package supply capabilities and deep integration into regional production networks, which Ethiopian firms lacked (Frederick & Staritz, 2012). Ethiopian manufacturers, in contrast, were often unable to ensure consistent quality and on-time delivery for large orders. This failure to meet the basic operational and relational standards required by modern apparel GVCs, as outlined by Azmeh and Nadvi (2014), led to a loss of confidence among international buyers and a consequent decline in orders and market share.

4. Domestic Instability and Macroeconomic Challenges

From the late 2010s onward, the sector was severely undermined by a confluence of domestic instability and profound macroeconomic challenges. Widespread social unrest and frequent protests directly disrupted critical logistics networks, including livestock supply chains and transportation, leading to significant operational halts (ICG, 2021). Compounding these supply-side issues, a crippling foreign exchange shortage severely constrained manufacturers' capacity to procure essential imported inputs, such as industrial chemicals, spare parts, and machinery. This constraint forced a large portion of the sector to operate significantly below production capacity, stifling output and efficiency (World Bank, 2020). Furthermore, the sector's international cost competitiveness was eroded by persistently high inflation, which disproportionately affected the costs of utilities and labor (CBE, 2022). Collectively, these interconnected crises political instability, foreign exchange illiquidity, and inflationary pressures generated a pervasive climate of uncertainty. This environment deterred crucial domestic and foreign direct investment at a pivotal juncture, thereby obstructing the capital infusion necessary for the sector's modernization and long-term recovery (Alemu & Mengistu, 2019).

3. Breakdown of the Decline within the Ethiopian Leather Sector

The Ethiopian leather industry, once a cornerstone of the country's industrialization strategy, has experienced a significant and multifaceted decline over the past few decades. This downturn can be analyzed by examining the specific struggles within the sector's value chain and the underlying reasons for its poor market performance.

I. Breakdown of the Sector's Weaknesses

The sector's fragility is evident at every stage of the value chain, from raw material to finished product.

A. Raw Material (Hide and Skin) Supply:

Of the various challenges constraining the performance of the leather manufacturing sector, the most foundational and debilitating weaknesses are located within the initial stage of the value chain: the supply of raw hides and skins. The sector's potential is fundamentally undermined by two interconnected issues: the poor quality of the raw materials and the fragmented, inefficient nature of their collection and initial processing.

The primary obstacle to producing high-quality leather goods is the pervasive prevalence of pre-slaughter and post-slaughter defects on hides and skins. As noted by Mekonnen, Tolera, and Senbeta (2012, p. 104), "defects such as branding, scratches, and tick damages significantly reduce the quality and value of hides and skins." These flaws are not incidental but are direct consequences of systemic failures. Poor animal husbandry practices, including inadequate control of parasites and exposure to harsh environmental elements like thorny bushes, directly cause scratches and tick damage (Mekonnen et al., 2012). Furthermore, the traditional practice of owner-branding animals for identification permanently scars the hide, drastically reducing its usable area and value. The problem is compounded by rough handling during the transportation of live animals to market and finally to slaughterhouses.

The degradation of raw material quality continues at the slaughtering stage, which is often the most critical point of damage. Many abattoirs, particularly in developing leather-producing nations, are characterized by unhygienic conditions and a lack of modern, humane slaughtering facilities. The use of blunt knives and unskilled personnel leads to deep flay cuts, score marks, and holes, which severely downgrade the hide (Ayele, 2018). As Beyan, Sirage, and Satheesh (2020, p. 45) emphasize, "The method of flaying, whether by manual or mechanical means, greatly influences the occurrence of defects like flesh remains and improper shape." The lack of immediate post-slaughter preservation infrastructure exacerbates the problem. Without prompt salting or chilling, hides begin to putrefy, leading to hair slip and bacterial damage, which renders them unsuitable for the production of high-grade leather.

Compounding the quality issue is the inherent inefficiency and fragmentation of the raw material supply chain. The collection of hides and skins from a vast number of small-scale, scattered slaughter points including rural areas and informal settings makes quality control and the implementation of standardized procedures nearly impossible. This fragmented system creates a high-cost, low-reliability procurement environment for tanneries. A study on the Ethiopian leather industry, which faces challenges representative of many others, highlighted that "the traditional marketing system is characterized by a long chain of intermediaries, which increases the cost of raw hides and skins and reduces the profit margin for primary suppliers" (Gebremariam, 2016, p. 112). This complex network of middlemen dis incentivizes quality-based pricing at the source, as pastoralists and farmers rarely receive a premium for better-handled animals, thus perpetuating the cycle of poor practice.

B. Manufacturing and Processing:

The manufacturing and processing segment within the leather industry is critically hampered by the widespread use of outdated technology and systemic inefficiencies. Numerous tanneries and footwear factories operate with machinery that is several decades old, a key factor leading to chronically low productivity, high production costs, and inconsistent product quality (Gebreeyesus, 2016; Geda & Seid, 2015). This technological stagnation has prevented the sector from moving significantly up the value chain, as evidenced by the persistent dominance of semi-processed (wet-blue) leather exports over high-value finished products. This failure to advance is a recurring theme in the literature. As Gebreeyesus (2016) observes, despite longstanding policy intentions, "The export structure remained dominated by semi-processed leather (wet-blue), indicating a failure in achieving the value addition target" (p. 18). This lack of vertical integration is further exacerbated by a shortage of skilled labor capable of operating modern machinery and managing complex production processes for finished goods (Mekonnen et al., 2017). Consequently, the sector remains trapped in a low-value-added equilibrium, unable to capture the higher margins associated with finished leather products.

C. Marketing and Export Performance:

The export performance of the Ethiopian leather sector has been characterized by volatility and a general declining trend, largely attributable to intensified global competition. As noted in a comprehensive sectoral analysis, Ethiopian leather products frequently struggle to comply with the stringent quality, consistency, and volume demands of major international buyers (Gebreeyesus & Iizuka, 2012). This non-compliance is a significant barrier to market entry and retention. A primary factor contributing to this challenge is the sector's historical focus on low-value-added items, such as semi-finished crust leather, rather than high-value finished products like footwear and leather goods (Mekonnen et al., 2017). This product concentration confines the sector to the lower, more competitive tiers of the global value chain.

Furthermore, the sector suffers from a pronounced lack of strong branding and targeted marketing strategies. Without a distinct brand identity to command consumer loyalty or justify price premiums, Ethiopian firms are forced to compete primarily on cost (Gebreeyesus, 2016). This positioning makes the sector particularly vulnerable to global price fluctuations and aggressive competition from more efficient, large-scale producers in Asia, who benefit from advanced technology, integrated supply chains, and economies of scale (Lall, 2000). Consequently, the inability to move up the value chain through branding and quality enhancement perpetuates a cycle of low returns and market instability.

II. Reasons for the Market Decline

The weaknesses within the sector's value chain are symptoms of deeper, systemic problems.

A. Policy and Regulatory Instability:

A primary driver of the Ethiopian leather sector's decline has been profound policy and regulatory instability. Frequent and often unpredictable shifts in government policy have created an environment of significant investment risk, deterring both domestic and foreign capital. A pivotal example was the government's decision to impose an export ban on raw hides and wet-blue leather, a strategy intended to force local value addition by mandating that all hides be processed into finished goods within the country. However, this policy was implemented without a concomitant effort to prepare the domestic manufacturing sector for this transition. As Lange et al. (2020) argue, such "local content policies" often fail when they are not "complemented by investments in productive capabilities and infrastructure" (p. 13). The Ethiopian context exemplifies this failure; the domestic industry lacked the consistent energy supply, chemical inputs, skilled labor, and financial capital necessary to competitively produce finished leather goods at a global standard (Gebreeyesus & Mohnen, 2013).

Consequently, the policy had distortive effects. It effectively penalized tanneries that had developed a competitive advantage and established market share in semi-processed (wet-blue) exports, while simultaneously propping up less efficient, domestically focused finished goods producers. This reduction in competitive pressure and the inability to export a higher-volume product led to a decline in overall sector efficiency and profitability. This aligns with the broader economic principle that export restrictions can reduce industry revenue and stifle growth by creating domestic market distortions (Piermartini, 2004). Therefore, the well-intentioned but poorly sequenced and supported policy intervention, rather than catalyzing upgrading, contributed significantly to reducing the overall international competitiveness of the Ethiopian leather sector.

B. Inadequate Infrastructure and Inputs:

The sector's competitiveness is severely hampered by chronic infrastructural deficits. A primary constraint is the unreliable provision of essential utilities. Manufacturers face frequent production stoppages due to an unreliable electricity supply and water shortages, which disrupt tanning and finishing processes, leading to inconsistent quality and delayed order fulfillment (Gebremeskel et al., 2020). These utilities are the lifeblood of leather processing, and their inconsistency directly increases operational costs and diminishes reliability in the eyes of international buyers.

Compounding these issues are poor logistics and transportation networks. Inefficient transport systems cause delays in both receiving raw materials and shipping finished goods, increasing lead times and costs (Mekonnen & Tilahun, 2021). This logistical bottleneck diminishes the sector's ability to operate on a just-in-time basis, a critical requirement in the fast-paced global fashion and automotive industries.

Furthermore, the sector is constrained by underdeveloped domestic market for critical production inputs. There is a significant lack of a local supply base for chemicals, dyes, and quality machinery parts (MoLSA, 2019). This deficiency forces manufacturers to rely exclusively on expensive and slow imports, which subjects them to volatile global prices, complex customs procedures, and long waiting periods for essential supplies (Gebreeyesus, 2016). This reliance on imported inputs not only inflates production costs but also creates a vulnerable and inflexible supply chain, further eroding the price and quality competitiveness of Ethiopian leather goods in the international market.

C. Lack of Finance and Investment:

Access to finance is a severe and widely documented constraint for firms in the Ethiopian leather industry. Both tanneries and manufacturers consistently struggle to secure affordable long-term loans, which are critical for two primary purposes: financing technological upgrading to meet international quality standards and covering essential working capital for daily operations (Gebreeyesus & Mohnen, 2013; Tilahun & Temesgen, 2021). The prevailing high-interest rates offered by commercial banks make such investments prohibitively expensive, crippling the sector's ability to modernize and compete globally.

This financial environment significantly deters both domestic and foreign direct investment (FDI). The perceived high risk of the manufacturing sector, coupled with institutional and regulatory hurdles, makes it an unattractive destination for the capital necessary for transformative growth (Oqubay, 2015). This lack of FDI is particularly detrimental, as it is a crucial conduit for bringing in not only capital but also modern technology, advanced management skills, and, most importantly, direct access to sophisticated international markets (UNIDO, 2017). Consequently, the sector remains trapped in a cycle of low investment, outdated production methods, and an inability to move up the value chain, directly contributing to its overall market decline.

D. Intense Global Competition and Shifting Markets:

The global leather market is characterized by intense competition, which has proven challenging for emerging producers. Established manufacturing hubs in Asia, particularly China, India, Vietnam, and Bangladesh, have secured dominant positions in the global value chain. These countries leverage massive economies of scale, highly integrated and efficient supply chains, and, crucially, consistent and strong government support in the form of subsidies, tax incentives, and infrastructure development (Gebreeyesus, 2016; UNIDO, 2017). In contrast, Ethiopian firms are predominantly small-scale and suffer from high production costs, making it difficult for them to compete on price, volume, or consistency with these established giants (Mekonnen et al., 2017).

Furthermore, the sector faces a significant external challenge from shifting global consumer preferences. A growing movement towards synthetic and vegan leather alternatives, driven by concerns over animal welfare and the environmental impact of traditional tanning, has begun to erode the market share of traditional leather goods (PETA, 2021; Saha et al., 2021). This trend presents a structural market shift that the Ethiopian leather sector, which is primarily focused on overcoming basic production and quality hurdles, is currently ill-equipped to handle, thereby exacerbating its market decline (Gebreeyesus, 2016).

E. Macroeconomic Challenges:

The performance of the Ethiopian leather sector is intrinsically linked to the country's broader macroeconomic environment. Recent years have been characterized by significant instability, with rampant inflation and a severe foreign exchange (forex) shortage acting as primary drivers of the sector's decline. These twin challenges cripple both the cost structure of domestic production and the capacity to access vital imported inputs, leading to a severe deterioration in competitiveness and market share.

1. Rampant Inflation and the Squeeze on Domestic Production

Ethiopia has experienced persistently high inflation, particularly in food and non-food prices, which has created a hostile environment for cost-sensitive sectors (World Bank, 2022). This inflationary pressure critically operates through two main channels to constrain domestic production. First, the rising costs of domestic inputs, from raw hides and chemicals to energy and transportation, directly increase the cost of goods sold, eroding profit margins (Geda & Yimer, 2016). Second, as the cost of living surges, pressure mounts for increased nominal wages to maintain workers' real incomes. This leads to increased labor costs for firms, which, when coupled with low productivity, further diminishes international competitiveness and squeezes domestic production capabilities (Alemayehu & Bekele, 2015).

The cost of raw hides and skins, the primary domestic input, is highly susceptible to broader price levels. As Gebreeyesus (2013) notes, even in periods of lower inflation, the informal and unregulated nature of raw material markets in Ethiopia leads to price volatility and quality issues. In a high-inflation environment, these problems are exacerbated, directly increasing the production cost for tanneries. Furthermore, inflation erodes real wages, forcing businesses to increase nominal wages to retain workers, thereby escalating labor costs. This overall increase in the cost of doing business without a commensurate increase in productivity or output price makes Ethiopian leather goods less competitive in international markets. As observed by Oqubay (2015) in his analysis of Ethiopian industrialization, sustaining competitive production costs is a fundamental challenge for export-oriented sectors, and macroeconomic instability directly undermines this.

2. The Foreign Exchange Crunch and Crippling of Industrial Capacity

The foreign exchange crunch represents one of the most direct macroeconomic constraints crippling the Ethiopian leather industry. The sector is heavily reliant on imported materials and capital goods, including critical chemicals (e.g., tanning agents, dyes, and fat liquors), spare parts for machinery, and modern equipment. This dependency creates a vulnerability to macroeconomic instability, particularly foreign exchange shortages (Oqubay, 2015). The prevailing forex crunch makes it nearly impossible for firms to reliably procure these essential inputs, leading to frequent production stoppages and chronic underutilization of installed capacity. This phenomenon aligns with the broader finding that foreign exchange rationing in import-dependent developing economies acts as a severe supply-side constraint, disrupting production schedules and hindering industrial growth (Stewart, 2017). Consequently, the inability to access foreign exchange for critical imports not only stifles current production but also prevents the technological upgrading necessary to remain competitive in the global leather market (Gebreeyesus, 2011).

This shortage has a cascading effect. First, it leads to production stoppages and underutilization of capacity. Without a steady supply of imported chemicals, the tanning process itself cannot continue. As Mekonnen et al. (2021) highlight, the lack of access to foreign exchange for importing essential production inputs is a "binding constraint" that forces firms to operate far below their installed capacity. Second, it cripples quality control and the ability to upgrade. The inability to import spare parts leads to machinery breakdowns and inefficiencies, while the blockade on modern machinery imports prevents technological upgrading. Consequently, the quality and consistency of Ethiopian leather products fall below international standards, leading to rejected orders and a loss of reputation among global buyers. This aligns with the findings of Tegegne (2017), who argues that the forex shortage not only stifles current production but also "impedes the sector's technological learning and capability development," locking it into low-value-added activities.

Conclusion And Recommendation

Conclusion

The Ethiopian leather industry stands at a pivotal juncture, shaped by the powerful confluence of innovation, digitalization, and a new wave of entrepreneurship. The traditional model, once reliant on raw material export and standardized manufacturing, is being fundamentally disrupted. The integration of advanced technologies, such as CAD/CAM for design and automated cutting systems, is no longer a luxury but a necessity for enhancing productivity, quality, and global competitiveness (Gebremeskel, 2021). Concurrently, digitalization is reconfiguring value chains, from e-commerce platforms enabling market access for small and medium enterprises (SMEs) to digital marketing strategies that allow brands to tell a uniquely Ethiopian story to a global audience (Abebe & Teka, 2020).

Crucially, this technological shift is being driven by a burgeoning entrepreneurial ecosystem. A new generation of entrepreneurs is moving beyond the export of semi-finished hides, focusing instead on creating high-value, branded finished products that fuse international design aesthetics with rich Ethiopian cultural heritage (Mekonnen & Tilahun, 2022). This "new wave" is challenging incumbents and creating a more dynamic and diversified industrial landscape. However, as Atnafu and Balda (2019) caution, the full potential of these trends can only be realized by addressing persistent structural challenges, including infrastructure deficits, access to finance, and skill gaps in digital literacy and advanced manufacturing. In essence, the emerging trends represent a paradigm shift from a commodity-based to a knowledge and value-driven industry, positioning entrepreneurship and digital tools as the central engines for future growth and sustainable development.

Recommendations

To harness the momentum of these emerging trends and ensure their sustainable integration, a multi-stakeholder approach is imperative. The following recommendations are proposed:

For Policymakers and Government Agencies:

For Financial Institutions:

For Industry Associations and Entrepreneurs:

For Academic and Research Institutions:

Acknowledgements

Leather and Leather Products Industry Research and Development Center (LLPIRDC) is acknowledged for providing every opportunity to pursue this review study.

Conflict Of Interest: The author declares that there is no conflict of interest in publishing and authorship of this manuscript.

Open Access By Aditum Open Access Journals id licensed under Creative Commons Attribution 4.0 International License. Based On a Work at aditum.org