Journal of International Research and Reviews

OPEN ACCESS | Volume 2 - Issue 1 - 2026

ISSN No: 3068-370X | Journal DOI: 10.61148/3068-370X/JIRR

Orekan, Atinuke Adebimpe

Department Of Estate Management, College of Environmental Sciences, Bells University of Technology, Ota, Ogun State, Nigeria.

*Corresponding author: Orekan, Atinuke Adebimpe, Department Of Estate Management, College of Environmental Sciences, Bells University of Technology, Ota, Ogun State, Nigeria.

Received: April 02, 2026 | Accepted: April 15, 2026 | Published: April 20, 2026

Citation: Orekan, Atinuke Adebimpe. (2026) “Department Of Estate Management, College of Environmental Sciences, Bells University of Technology, Ota, Ogun State, Nigeria”, Journal of International Research and Reviews, 1(2); DOI: 10.61148/3068-370X/JIRR/008.

Copyright: © 2026. Orekan, Atinuke Adebimpe. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

Urbanization poses significant challenges for cities, including population growth, limited resources, and environmental concerns. This systematic literature review delved into the underlying framework as a basis for understanding the potential effectiveness of land tax in promoting sustainable urban development and shaping land use pattern. In addition, the study examines the theoretical insights under some basic elements; which are economic rationale, land value capture, spatial planning and zoning. The study underscores the benefits that contributes to the sustainable urban development. All these were achievable with a structured methodology involving systematic strategies, screening processes and quality assessment. In achieving this, a reviewed research questions regarding its sustainability as a regulatory tool were examined; some of which were how theories on land tax contribute to its effectiveness and how land tax promotes the sustainability of urban development. This study helps researchers, legislators, and government agencies manage the difficult obstacles associated with using land tax as a regulatory tool by summarizing the body of available evidence.

Land Tax, Regulatory tool, urban development, Sustainability

1.0 Introduction

Due to the various difficulties that come with the world's cities' increasing urbanization, urban development is an important worldwide concern (Follmann, Willkomm & Dannenberg, 2021). Numerous socio-economic and environmental issues, such as population increase, few resources, poor infrastructure, a lack of housing, traffic jams, and environmental degradation, have been brought on by the extraordinary expansion of metropolitan areas (Zhang, 2016; Follmann et al., 2021). In order to solve these issues and direct urban development toward sustainability, effective regulatory measures are required.

Given that Nigeria is one of the most populous countries in Africa and is rapidly becoming more urbanized, the issues associated with urban development are especially acute. Nigerian cities are facing a number of challenges, including the burden on vital services, informal settlements, fast population expansion, and inadequate urban infrastructure (Aliyu & Amadu, 2017). They further affirmed that these challenges have intensified the need for effective regulatory mechanisms that can guide urban development in a sustainable and inclusive manner.

According to Franzen and McClucskey (2017), Land tax is a recurrent tax on the ownership of undeveloped or developed land, excluding any development made on land. Land taxes can be classified into two: Property tax and Land charges. Examples of land charges are ground rent, land use charges and fees such as: survey, registration and search, valuation, application, application, re-grant, change of purpose and occupancy permit.

Property tax is a charge levied compulsorily on interest in ownership and use of landed properties. This includes: tenement rate, probate tax, capital gains tax, capital transfer tax, stamp duties, withholding tax, severance tax, betterment/development tax and site-value tax. It is a major avenue for realizing income for local and state authority.

Furthermore, land tax is one of the regulatory measures that has drawn attention in the development of urban growth. According to Nassios et al. (2017), property taxes entails charging landowners according to the worth of their assets. According to Nassios et al. (2017), it is a multipronged strategy that seeks to reduce the negative effects of urban sprawl, influence land use patterns, encourage efficient land utilization, discourage speculation, and create cash for urban infrastructure. In view of this, this study examined ways in which land tax discourages speculation, increase revenue generation and address environmental and social concerns.

2.1 Unveiling Land Tax: A theoretical insight behind land tax as a regulatory tool for Urban development

This study delve into the underlying insight as a basis for understanding the potential effectiveness of land tax in shaping land use pattern, promoting sustainable urban development and addressing the challenges associated with urbanization. The theoretical framework of this study provides some basic key elements and these are; Economic Rationale, Land Value Capture, Spatial Planning and Zoning, Externalities and Market Failures, Social Equity and Inclusivity. By integrating these theoretical perspectives, researchers gain a comprehensive understanding of the underlying mechanisms Land tax is grounded in economic principles that aim to align land use decisions with market forces and efficient resource allocation (Levine, 2010). It is predicated on the idea that a piece of land's location and possible uses affect its value. Taxing land allows governments to prevent speculative activity, encourage landowners to use their property wisely, and promote productive land use. In view of this, land tax operates on the principle of capturing the rise in land value brought about by public spending, better infrastructure, and urban planning initiatives (Chi-Man Hui et al., 2004; Medda, 2012). Therefore, land value acknowledges that public investments frequently result in an increase in land values and works to guarantee that landowners use taxes to return a fair portion of these gains to the community (Chi-Man Hui et al., 2004). Sustainable urban growth can be encouraged by adopting land value capture techniques to finance public amenities, affordable housing, and urban infrastructure.

Zoning laws and land taxation are intimately related to one other. Certain land uses, such as residential, commercial, or industrial, are designated inside designated zones by zoning restrictions. In order to influence land use decisions and promote the intended development patterns, property taxes can be crafted to comply with these zoning restrictions (Downs, 2010;

Wenner, The zoning and spatial planning 31 rules provide another crucial theoretical foundation for land taxation.

Zoning laws and spatial planning can be incorporated into land tax design to influence land use decisions and promote desired development patterns (Downs, 2010; Wenner, 2018). Policymakers can promote sustainable urban forms and reduce sprawl by directing urban expansion towards compact, mixed-use, and transit-oriented development by varying tax rates according to land use classifications.

Furthermore, land taxation acknowledges the presence of market failures and externalities in urban growth (Lai, 2011). When a landowner's actions affect other landowners or the community at large, this is known as an externality. For instance, the neighboring areas may be financially impacted by traffic congestion or environmental pollution brought on by specific land uses (Caldari, & Masini, 2011). By internalizing these external expenses and encouraging landowners to adopt more environmentally friendly methods, land taxes help reduce the negative externalities brought on by urban expansion.

These theories of land taxes offer a foundation for comprehending the fundamental ideas and workings that underlie the ability of land taxes to affect land use patterns, encourage sustainable urban growth, and deal with the problems brought on by urbanization. Policymakers and urban planners can create efficient land tax systems that support more sustainable and inclusive cities and are in line with larger urban development objectives by taking these theoretical underpinnings into account.

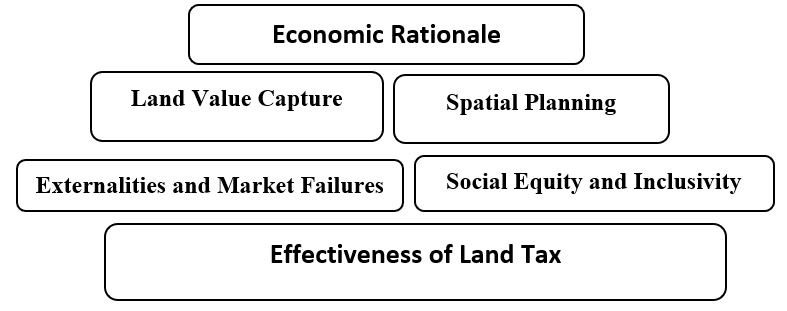

Fig 1: conceptual Framework (Source: Researcher, 2024)

The main elements of the framework are depicted in the diagram. The cornerstone is the economic justification, which emphasizes the concepts of effective resource allocation and market dynamics. The framework incorporates several concepts such as land value capture, social equity, market failures, externalities, and spatial planning, all of which build upon this basis. The interaction between these components contributes to the effectiveness of land tax as a regulatory tool for urban development. The framework recognizes the interconnections and dependencies between these elements, demonstrating how land tax can influence land use patterns, capture the value generated by public investments, shape spatial planning decisions, internalize external costs, and promote social equity.

Please note that the diagram provides a simplified visual representation of the theoretical framework. In practice, the relationships and interactions between these components are more complex and multidimensional. Nonetheless, the diagram serves to convey the overarching structure and concepts of the framework.

2.2 Benefits of Land Tax as a Regulatory Tool

Land taxation is being implemented in different forms in various countries. Certain nations impose taxes just on land, whereas others impose taxes on both land and improvements, while some countries concentrate on only the buildings. Birds and slack (2003) gave examples of different countries with their ways of implementing land tax. According to them, country like Kenya and some part of Australia and South Africa tax only the land portion of the property, while countries like Tanzania tax only buildings. Nuhu (2010), from his own opinion, classified land tax to be in two forms; one based on the valuations of buildings and the other on land. At the moment, the former is being used in Abuja, Nigeria. There is a crucial difference between the two systems since these systems have one on building values and the other on land values. The distinction between the two systems is an important one, as these systems have significantly different impacts on incentive motives and development results. He further explained that tax is decreased or removed from income on buildings, thereby giving the incentive to maintain, restore and improve properties. Meanwhile land value tax is different from this because it is a tax on an unimproved value of land only.

Land tax as a regulatory tool offers several benefits that contribute to sustainable urban development. These benefits include:

All things considered, the regulatory instrument of land taxation provides a number of advantages that support sustainable urban growth. Land taxes can help transform urban areas into more sustainable, inclusive, and dynamic places to live and work by tackling urban sprawl, promoting efficient land use, deterring speculation, raising funds for infrastructure, and reducing environmental and social 10 effects.

2.3 Navigating the Land Tax Maze

Although there are potential advantages to land taxation, there are also significant drawbacks and difficulties. These include political opposition, public perception, potential negative effects on specific groups and property owners, administrative complexity and implementation issues, and political resistance. To administer a successful land tax system, there must be strong administrative capacity, including precise property assessment, effective tax collection systems, and enforcement protocols. It can be difficult to set up an impartial and open assessment procedure, especially when there are gaps in or out-of-date land records. Sufficient resources and training for tax authorities are imperative to guarantee seamless execution and mitigate administrative strains on property proprietors. However, there are numerous restrictions affecting the effectiveness of land tax as a regulatory tool and these are discussed as;

2.4 Critical Analysis of the Evaluation of the Effectiveness of Land Tax

A thorough analysis of the land tax's effects on many facets of urbanization is necessary to determine how effective it is as a regulatory tool for urban development. When assessing the efficacy of land taxation, the following factors may be taken into account:

Its significance for land use and development patterns is indicated by an evaluation of the impact of land taxation on land use patterns, such as supporting compact, mixed-use development, decreasing sprawl, and promoting efficient land utilization. In determining its efficacy, it is also important to determine how much land tax policies have impacted land use variety, density, and development choices.

This in turn aids in estimating the amount of money generated by land taxes for the construction of urban infrastructure. One possible next step would be to assess if the income is in line with the objectives of urban development and adequately fills up financing shortfalls.

The affordability of housing and the availability of housing become significant determinants of how successful land taxes are as regulatory instruments. There should be proof accessible on whether land tax laws have promoted the development of reasonably priced housing, curbed speculation, or expanded the pool of available housing options. Evaluate how well the land tax works to alleviate the housing crisis and increase affordability for different income levels.

Determining the efficacy of land taxes in reducing the negative social and environmental effects of urbanization is essential. Its influence on environmental and social welfare will be determined by evaluating whether land tax policies have helped to promote social justice, encourage sustainable land use practices, and lessen environmental deterioration. Analyze the degree to which land taxes have encouraged landowners and developers to embrace ecologically sustainable methods and support social welfare.

Property owners' compliance rates will be determined by the efficiency of the administrative framework for implementing land tax policies, as well as the effectiveness of property valuation techniques, tax collection methods, and enforcement procedures. These factors will also reveal any administrative obstacles that may impede the successful implementation of land tax.

Policymakers and scholars can determine the overall efficacy of land taxes as a regulatory instrument for urban growth by analyzing these factors. Both qualitative elements, like stakeholder perspectives and social justice outcomes, and quantitative indicators, such revenue creation and land use patterns, should be taken into account in the review. The evaluation's conclusions can guide changes to policies and point out areas that still need work to increase the efficiency of land taxes in encouraging sustainable urban growth.

2.6 Policy Recommendations and Future Directions

Based on the evaluation of the effectiveness of land tax as a regulatory tool for urban development, the following policy recommendations and future directions can be considered:

By implementing these policy recommendations and pursuing future directions, Nigeria can maximize the effectiveness of land tax as a regulatory tool for urban development. These actions can contribute to sustainable land use, affordable housing provision, equitable development, and the overall improvement of urban environments in Nigeria.

3.0 Methodology

The goal of this study was to thoroughly investigate the theoretical underpinnings of land taxation as a regulatory tool and any potential connections to the results of urban growth. In doing so, the review tackled significant research problems including its applicability as an urban development regulation tool, its constraints and challenges, possible adverse effects on particular populations, political opposition, and insufficient evaluation procedures.

3.01Search Strategy

In order to guarantee a thorough exploration of pertinent literature, databases including Scopus, Web of Science, and Google Scholar were closely examined for the search. Boolean operators were used to combine keywords like "land value," "regulatory tool," "revenue generation," "land use," and "land development" to narrow down search queries.

3.02 Screening, Selection and Data Extraction

The titles and abstracts of pertinent papers were used to conduct the screening process. They underwent a thorough assessment of relevance and quality during full-text screening. Data were extracted to systematically record information on research problem, methodology, key findings and conclusions. Consistency in data extraction was ensured through clear definitions and guidelines.

The quality of data from relevant study was also evaluated. Study design, sample size and data collection methods were considered to ensure the validity and reliability of findings.

3.03 Synthesis and Analysis

Findings from included studies were synthesized using synthesis techniques. Common themes, patterns, and discrepancies across studies were identified and analyzed. Subgroup analyses were conducted to explore variations in study characteristics or findings.

3.04 Interpretation and Conclusion

The synthesized findings were interpreted in the context of research questions, discussing their implications for theory, practice and policy. Gaps in the literature were identified, and directions for future research were proposed based on the review findings.

4.0 Report

A robust report was created utilizing 25 Meta-Analytic elements and the recommended reporting items for the systematic review guideline as a standard. This has enabled the report to be transparent in line of search approach, selection standards, extraction of data, evaluation of quality, and synthesis methods and interpretation of findings.

5.0 Conclusion, findings and Recommendation

To sum up, land taxes have shown to be an effective regulatory instrument for encouraging sustainable urban growth. Several important conclusions are drawn from the theoretical framework analysis, case studies, and effectiveness evaluation:

First off, by discouraging underutilization and property speculation, land taxes can successfully promote efficient land use and growth. Land taxes encourage landowners to make the best use of their properties by levying taxes based on land value. This promotes compact, mixed-use development and slows urban sprawl.

Second, land taxes fill financing shortages and encourage the supply of basic amenities by generating income for municipal infrastructure and services. Land taxes guarantee that landowners give back a fair portion to the community by collecting the rise in land value brought about by public investments, so promoting sustainable urban growth.

Thirdly, one important tool for tackling the issue of home affordability is the land tax. Land taxes can encourage the productive use of properties through mechanisms like development charges or vacant property taxes. This will increase the supply of housing and decrease speculation, which will ultimately improve affordability and provide fair access to housing.

Even though land taxes have many advantages, there are a number of restrictions and difficulties that need to be resolved. Political opposition, possible adverse effects on particular groups, and administrative difficulties must all be carefully taken into account while implementing. To maximize the efficiency of land tax, adequate assessment procedures, stakeholder involvement, and cooperation with other policies are essential.

In conclusion, land taxes have the potential to be a useful regulatory tool for urban growth if they are customized for local contexts and supported by laws. It is a useful tool in the pursuit of urban development objectives because of its capacity to influence land use patterns, produce income, solve issues of affordability, and support inclusive and sustainable cities. Ongoing observation, assessment, and adjustment are necessary to optimize the efficacy of land tax. Gaining knowledge from global experiences, like the Singaporean and Vancouver case studies, can help improve policies and offer insightful information about Nigeria's particular urban problems. Further research, knowledge sharing, and piloting of land tax initiatives can contribute to evidence-based policy development and implementation.

Nigeria may maximize the potential of this regulatory tool by utilizing the advantages of land tax, resolving its drawbacks, and incorporating it into an all-encompassing urban development plan. Nigeria can harness the potential of this regulatory tool to create sustainable, inclusive, and thriving cities for its residents.

Open Access By Aditum Open Access Journals id licensed under Creative Commons Attribution 4.0 International License. Based On a Work at aditum.org