International Journal of Business Research and Management

OPEN ACCESS | Volume 4 - Issue 3 - 2026

ISSN No: 3065-6753 | Journal DOI: 10.61148/3065-6753/IJBRM

Ubaydullaeva Aziza Khamraqul Qizi

PhD, Chief Specialist, Institute of Budget and Tax Studies.

*Corresponding Author: Ubaydullaeva Aziza Khamraqul Qizi, PhD, Chief Specialist, Institute of Budget and Tax Studies.

Received Date: June 02, 2026 | Accepted Date: June 22, 2026 | Published Date: July 01, 2026

Citation: Khamraqul Qizi UA., (2026). “The role of Excise Taxation in the Formation of Budget Revenues in Uzbekistan”. International Journal of Business Research and Management 4(5); DOI: 10.61148/3065-6753/IJBRM/087.

Copyright: © 2026. Ubaydullaeva Aziza Khamraqul qizi, Alejandro. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

The article examines the features of excise tax application in Uzbekistan's economy. During the "preparatory phase" of a country's accession to the World Trade Organization (WTO), governments typically revise their excise tax system to adapt it to the requirements of the organization. A forecast for revenue to the State Budget until 2030 years has been developed through the adjustment of excise tax rates. Revenue from excise taxes in Uzbekistan is expected to continue growing in the future if current demographic trends persist, unrecorded consumption decreases, and excise tax rates are carefully optimized, especially on high-income products. GDP is observed as a negative coefficient in 2 models, which may be related to a shift in consumption models (for example, towards informal channels) as incomes increase. The ways for modernizing excise tax in the national economy are justified. Recommendations for improving excise taxation are also provided. To reduce the negative health effects for individuals engaged in gambling and to increase budget revenues, it is proposed to introduce a tax on gambling activities.

excise tax, basics of excise taxation, Tax Code, tax incentives, human health, excisable goods, tax revenue, State Budget

In many countries around the world, there is a growing trend towards introducing indirect taxes on goods and services, in particular excise taxes on products whose excessive consumption has a negative impact on human health or is dangerous to the environment. According to the International Monetary Fund, “…in recent years, the global dynamics of budget revenues from taxes on goods and services in countries around the world has averaged 10% of GDP in Germany, 8.0–7.6% in Canada, 4.4–4.1% in the USA, and 7.5–8.2% in Russia [1]”. This situation demonstrates the high relevance of scientific and theoretical research in the field of excise taxes and their integration into national legislation, taking into account international requirements.

In scientific research conducted worldwide, the issues of increasing the socio-economic efficiency of excise tax, improving atmospheric air by enhancing its stimulating and restrictive functions, and enhancing its impact on reducing disease incidence are considered a global problem.

In Uzbekistan, special attention is being paid to improving the efficiency of excise taxes, optimizing and aligning rates on domestic and imported products, as well as improving the environmental situation and public health. In particular, the strategic objectives of the country's socio-economic development include "...full digitalization, simplification of the tax system, and the creation of equal opportunities for entrepreneurs," as well as "...reducing the proportion of overweight and obese adults to 32 and 23 percent, respectively..." as one of the priority areas[2].

In the modern world, the development of excise taxation is aimed, as a rule, at creating equal competitive conditions for domestic and foreign producers of excisable goods. At the same time, it is important for the government of any country to ensure the possibility of reimbursing excise taxes on the export of excisable goods in order to support the competitiveness of domestic producers in the world market. The solution to this problem creates conditions not only for improving the consumption of consumer goods by the population, but also, at the same time, additional opportunities are created to increase budget funds and ensure the stability of their receipt [11].

The concept of excise taxes is based on the principles of optimal taxation theory (Diamond & Mirrlees, 1971), which suggests that taxes should be structured to minimize economic distortions while maximizing revenue. Excise taxes are typically levied on goods with inelastic demand (e.g., alcohol, tobacco, fuel), ensuring a stable revenue stream with minimal impact on consumption [16].

Early systems of public finance focused on taxing income, consumption, and wealth (Authen, Rob, 1976) [3]. The most commonly identified principles of a good tax system are fairness, efficiency, adequacy, stability of revenue, and tax administration and compliance costs in line with economic reality.

The immediate implication for governments (such as states and provinces) is that probably the most appropriate source of revenue should be a "simple, single-step (preferably retail) sales tax (RST) collected directly from final (resident) consumers." consumers, and possibly some excise taxes" ( Musgrave, 1983 )[4].

The practical consequence of these tax concepts is that the analysis of the tax distribution system should cover the revenues of both the central government and local authorities (in Uzbekistan – the State Budget and local budgets). Tax researchers Bird R. and Gendron P. (2007) in their book “VAT in Developing and Transition Economies”[5] and economist, known for his research in the field of tax policy and distributional analysis, Creedy J. (1998), in his article “Excise Taxation in New Zealand”[6], expressed a common opinion that the purpose of excise tax is, including increasing revenue, corrective taxation to eliminate externalities, limiting the consumption of harmful goods.

Also, Patricia E. and Ray R. (2009) in their article "Taxation and the Household" discuss the purposes of introducing excise taxes, including revenue generation, the elimination of externalities, and their impact on household behavior and welfare. They analyze the consequences of introducing excise taxes for different types of households [17].

In recent years, the economy of the Republic of Uzbekistan has continued to implement measures aimed at forming a full-fledged market economy. The taxation of legal entities is being modernized, which has a positive effect on the dynamics of the main macroeconomic indicators. Thus, statistical data show that Uzbekistan's GDP in 2024, compared with 2023, increased in real terms by 6.5%, and the GDP deflator index, in relation to 2023 prices, amounted to 113.3%. In 2024, GDP per capita growth in real terms, compared with 2023, amounted to 4.4%. The share of industry in GDP amounted to 26.4% in 2024, and the share of services increased from 46.2% to 47.4%, which indicates positive dynamics.

At the same time, in recent years, negative trends have been observed in the economy of Uzbekistan. Thus, in 2023, the inflation rate in Uzbekistan was - 8.77%, and in 2024 - 9.8%. According to the results of 2024, the gross added value (GVA) of the informal and shadow economy of the Republic of Uzbekistan amounted to 505,650.1 billion soums, and its share in GDP was 34.8%.

Let's consider the trends in excise tax revenues to the State Budget of the Republic of Uzbekistan. To assess the excise tax, it is appropriate to consider the trends in excise tax revenues to the State Budget. (Table 1). Revenues to the State Budget (excluding the State Fund) from excise taxes increased from 10,314.7 billion soums in 2019 to 19,059.9 billion soums in 2024, or 1.84 times.

Table 1. nStructure of budget funds for indirect taxes, (billion soums)

|

|

2019 y. |

2020 y. |

2021 y. |

2022 y. |

2023 y. |

2024 y. |

|

Income (excluding GCF) – total |

112 165,4 |

132 900,7 |

164 680,3 |

201 863,8 |

231 721,3 |

274 422,7 |

|

Indirect taxes |

46 427,2 |

46 428,4 |

56 2901 |

71 390,2 |

83 325,8 |

88 340,9 |

|

VAT |

33 809,8 |

31 177,4 |

38 439 |

52 189,4 |

57 885,3 |

59 280,0 |

|

Excise tax |

10 314,7 |

11 721,2 |

13 100,8 |

13 455,0 |

15 834,4 |

19 059,9 |

|

Customs duty |

2 302,8 |

3 553,7 |

4 764,9 |

5 745,7 |

9 606,1 |

10 001 |

The decrease in the share of excise tax revenues to the State Budget is due to the elimination of the excise tax on the import of transports, which was implemented on August 1, 2020, as well as the elimination of 73 types of commodity items. [7].

The number of cases of diabetes, obesity, heart diseases and oncological diseases is growing in the republic. The state of the atmospheric air is deteriorating due to emissions of pollutants. The increase in the above-mentioned negative factors indicates that the current economic instruments, including excise taxes, are not yet bringing significant positive results in solving the above problems [17].

The head of state, Sh. Mirziyoyev, speaking at a meeting to discuss expected economic results on October 17, 2024, noted that foreign experts predict a deterioration in the situation in foreign export markets in 2025 due to increasing competition and instability in raw material prices. This could be a test for production volumes and export-oriented industries. In the context of maintaining the main tax rates, the only way to increase budget revenues is to improve tax administration. Therefore, structural changes should not occur through interference in the activities of entrepreneurs, but through digitalization, the introduction of artificial intelligence technologies and the legalization of the shadow economy[8].

In the sphere of excise taxation in the republic, there are still differences between the rates for domestic and imported products, there are no tax incentives to protect the quality of atmospheric air, healthy nutrition and lifestyle are not sufficiently supported, especially among young people. In this regard, the Parliament and the Government of the republic are taking additional measures to solve the above-mentioned social problems.

Thus, according to the Decree of the President of February 7, 2025, the State Program for 2025 was approved in the republic. It plans to implement practical measures for 2025 in 5 priority areas. It pays special attention to issues of improving public health and creating conditions for the formation of a healthy lifestyle.

The solution to this problem can be achieved by increasing the influence of excise taxation on the production and economic activities of entrepreneurs, legal entities and individuals, as well as on the consumption of food products by the population and the formation of a healthy lifestyle. To achieve these goals, it is advisable to update the existing excise taxation instruments and introduce new, more effective tax mechanisms.

The republic attaches great importance to improving the business environment and creates additional incentives for entrepreneurs. The "Development Strategy of the New Uzbekistan for 2022-2026", approved by the Decree of the President of the Republic of Uzbekistan dated January 29, 2022 No. UP-60, pays special attention to improving the efficiency of taxation, instruments for regulating business activities in the context of the transformation of the business environment[9].

The Development Strategy “Uzbekistan-2030”, which specifies and clarifies the objectives of the “Development Strategy of the New Uzbekistan for 2022-2026”, attaches great importance to the problem of increasing the average life expectancy of the population, reducing 2.5 times indicators of early mortality from oncological, cardiovascular and other diseases[10]. Also p.20 The Development Strategy " Uzbekistan-2030 " states that in order to form proper nutrition and a healthy lifestyle among the population, the incidence of overweight and obese adults should be reduced to 32% and 23%, respectively. The proportion of children under 5 years of age with obesity should be reduced by an average of 2 times [12].

The experience of a number of countries shows that excise taxes are an effective tool for reducing the consumption of dangerous drinks (if consumed in excess), in particular carbonated and non-carbonated sweet drinks. For example, in Italy, sales of sugar-sweetened drinks fell by an average of 7.7% in the first 4 months after the introduction of this tax, and in Chile, the purchase of sugary drinks fell by 22% [13].

Materials And Method

This report presents excise tax revenue forecasts for Uzbekistan until 2030 years, covering both domestic and imported excise tax revenues across different product categories. The forecasting approach is based on historical data and time series modeling techniques to provide accurate and reliable projections.

The forecast is based on historical excise tax revenue data from 2016 to 2024 for both domestically produced and imported products. The dataset includes revenue from Beer, Wine, Vodka/Cognac, and Cigarettes, covering:

Data Cleaning and Structuring

The datasets were cleaned and structured to ensure consistency in the forecasting model:

Why Holt-Winters Method?

To forecast excise tax revenues, we used the Holt-Winters Exponential Smoothing Model, a widely used time series forecasting technique. This method is effective for modeling:

How the Holt-Winters Model Works

The Holt-Winters method extends Simple Exponential Smoothing by adding components for trend and seasonality:

St=aYt+1-aSt-1+Tt-1

Tt=βSt-St-1+(1-β)Tt-1

Where:

= Level (smoothed value of the series at time t)

= Level (smoothed value of the series at time t) = Observed value at time t

= Observed value at time t = Trend (growth rate estimate)

= Trend (growth rate estimate)This model updates the trend and level for each year based on past trends, making it highly effective for financial and tax revenue forecasting.

Implementation Process

We will use three forecasting scenarios based on different economic and tax policy assumptions. These scenarios are designed to account for uncertainties such as economic growth, policy changes, inflation, and consumer behavior.

1. Moderate Scenario (Baseline Forecast)

2. Optimistic Scenario (High Growth)

3. Pessimistic Scenario (Low Growth)

Results And Discussion

In the course of the research, we developed a forecast for excise tax revenues until 2030 yeara. The Holt- Winters exponential smoothing model , which is a widely used method for time series analysis, was used to forecast excise tax revenues . Three forecasting scenarios were used in the analysis , based on different economic and fiscal policy assumptions: moderate, optimistic and pessimistic

Table 2. Domestic - Moderate Scenario

|

Year |

Beer |

Wine |

Strong drinks |

Cigarettes |

Total |

|

2025 |

500,70 |

16,64 |

2 000,04 |

2 862,76 |

5 380,14 |

|

2026 |

563,20 |

15,74 |

2 125,41 |

3 116,11 |

5 820,46 |

|

2027 |

625,07 |

14,85 |

2 249,10 |

3 366,92 |

6 255,94 |

|

2028 |

686,32 |

13,97 |

2 371,55 |

3 615,23 |

6 687,07 |

|

2029 |

746,95 |

13,10 |

2 492,77 |

3 861,05 |

7 113,87 |

|

2030 |

806,99 |

12,24 |

2 612,79 |

4 104,4 |

7 536,42 |

Import -Moderate Scenario

|

2025 |

21,35 |

16,58 |

36,44 |

868,87 |

943,24 |

|

2026 |

23,22 |

18,53 |

40,00 |

1 287,54 |

1 369,29 |

|

2027 |

25,08 |

20,46 |

43,64 |

1 702,16 |

1 791,34 |

|

2028 |

26,92 |

22,38 |

47,24 |

2 112,64 |

2 209,18 |

|

2029 |

28,74 |

24,27 |

50,77 |

2 519,01 |

2 622,79 |

|

2030 |

30,54 |

26,14 |

54,27 |

2 921,32 |

3 303,27 |

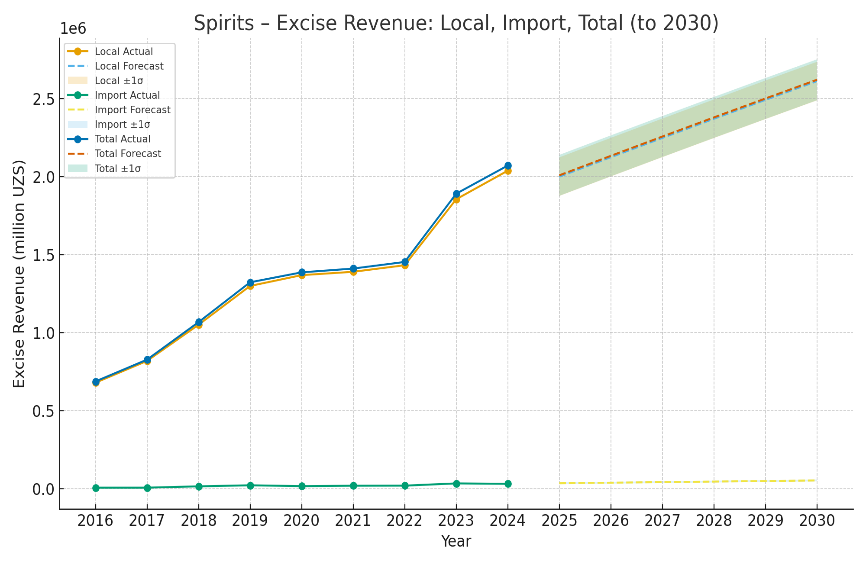

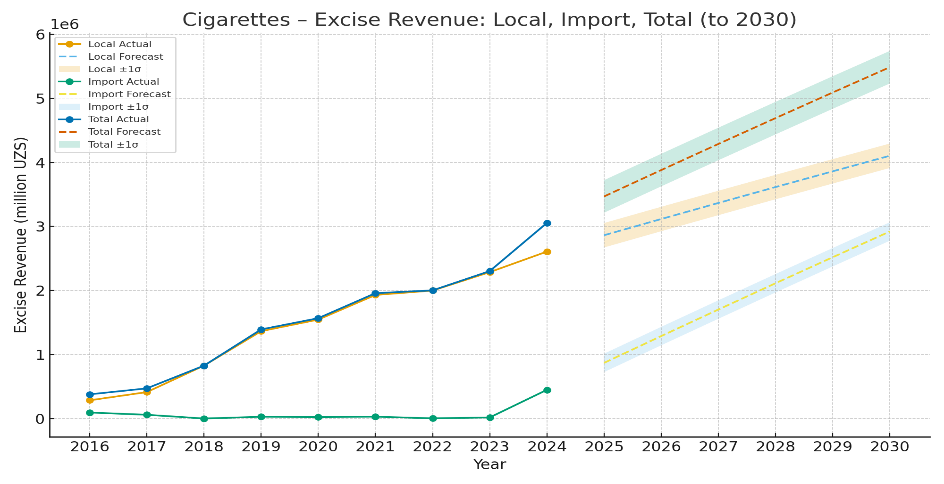

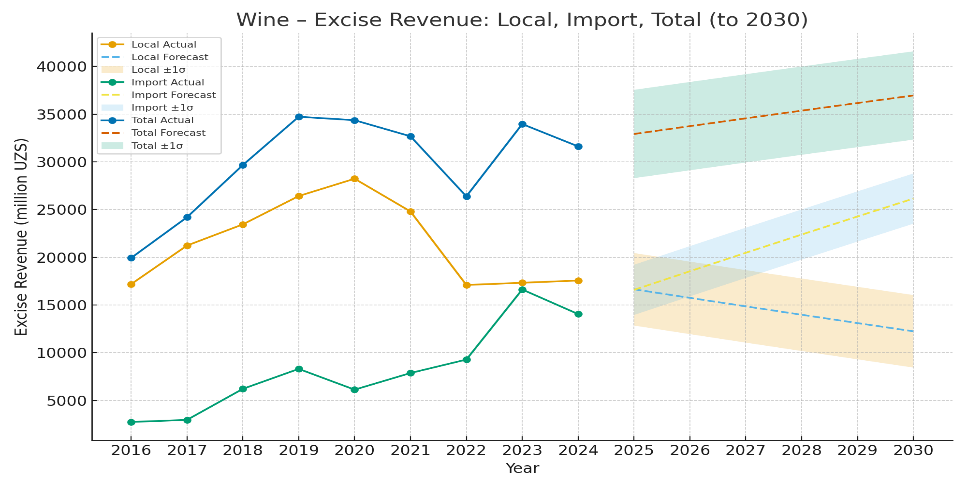

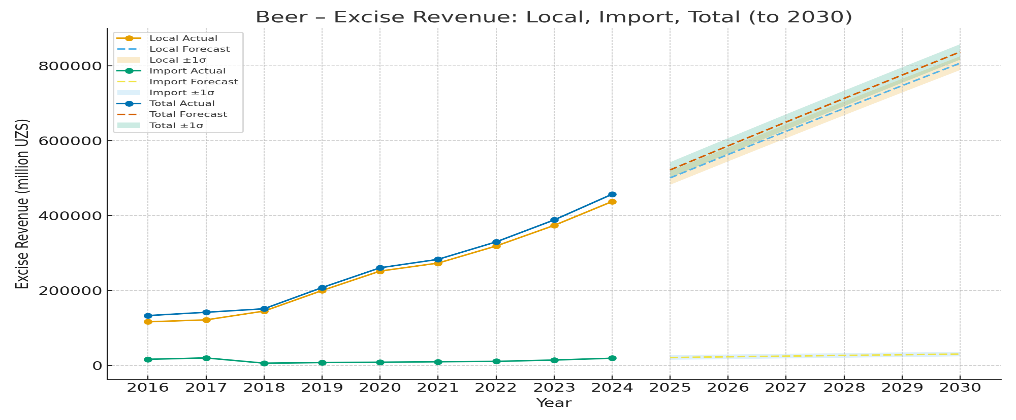

In Scenario 1 (baseline), excise tax revenues on domestic goods in 2030 will amount to 806.99 billion soums for beer, 12.24 billion soums for wine, 2,612.79 billion soums for spirits (vodka), and 4,104.4 billion soums for cigarettes, for a total of 7,536.42 billion soums.

In the same scenario, excise tax revenues on imports in 2030 will amount to 30.54 billion soums for beer, 26.14 billion soums for wine, 54.27 billion soums for spirits (vodka), and 2,921.32 billion soums for cigarettes, for a total of 3,303.27 billion soums.

Table 3. Optimistic scenario #2 for excise tax revenues (+10% growth), trillion soums

Domestic

|

Year |

Beer |

Wine |

Strong drinks |

Cigarettes |

Total |

|

2025 |

518,99 |

20,44 |

2 124,03 |

3 053,29 |

5 716,75 |

|

2026 |

581,49 |

19,54 |

2 248,97 |

3 306,64 |

6 156,64 |

|

2027 |

643,36 |

18,65 |

2 372,66 |

3 557,46 |

6 592,13 |

|

2028 |

704,61 |

17,77 |

2 495,11 |

3 805,77 |

7 099,49 |

|

2029 |

765,25 |

16,90 |

2 616,33 |

4 051,59 |

7 450,07 |

|

2030 |

825,28 |

16,04 |

2 736,35 |

4 294,96 |

7 872,63 |

Import

|

Year |

Beer |

Wine |

Strong drinks |

Cigarettes |

Total |

|

2025 |

27,45 |

19,21 |

42,06 |

1 012,24 |

1 100,96 |

|

2026 |

29,33 |

21,16 |

45,70 |

1 431,05 |

1 527,24 |

|

2027 |

31,18 |

23,09 |

49,30 |

1 845,68 |

1 949,25 |

|

2028 |

33,02 |

25,00 |

52,87 |

2 256,15 |

2 367,04 |

|

2029 |

34,84 |

26,90 |

56,40 |

2 662,52 |

2 780,66 |

|

2030 |

36,64 |

28,77 |

59,89 |

3 064,83 |

3 190,13 |

In Scenario 2 (optimistic, 10% growth), excise tax revenues on domestic goods in 2030 will amount to 825.28 billion soums for beer, 16.04 billion soums for wine, 2,736.35 billion soums for spirits (vodka), and 4,294.96 billion soums for cigarettes, for a total of 7,872.63 billion soums.

In this scenario, excise tax revenues on imports in 2030 will amount to 36.64 billion soums for beer, 28.77 billion soums for wine, 59.89 billion soums for spirits (vodka), and 3,064.83 billion soums for cigarettes, for a total of 3,190.13 billion soums.

Table 4.

Domestic - Pessimistic Scenario

|

Year |

Beer |

Wine |

Strong drinks |

Cigarettes |

Total |

|

2025 |

482,41 |

12,85 |

1 876,92 |

2 672,22 |

5 044,4 |

|

2026 |

544,91 |

11,95 |

2 001,85 |

2 925,57 |

5 484,2 |

|

2027 |

606,77 |

11,06 |

2 125,54 |

3 176,38 |

5 919,7 |

|

2028 |

668,03 |

10,18 |

2 247,91 |

3 424,69 |

6 350,8 |

|

2029 |

728,66 |

9,31 |

2 369,21 |

3 670,51 |

6 777,6 |

|

2030 |

788,70 |

8,44 |

2 489,23 |

3 913,88 |

7 200,2 |

Import

|

Year |

Beer |

Wine |

Strong drinks |

Cigarettes |

Total |

|

2025 |

15,25 |

13,95 |

30,82 |

725,21 |

785,23 |

|

2026 |

17,12 |

15,90 |

34,45 |

1 144,02 |

1 211,4 |

|

2027 |

18,98 |

17,84 |

38,06 |

1 558,64 |

1 633,5 |

|

2028 |

20,82 |

19,75 |

41,62 |

1 969,12 |

2 051,3 |

|

2029 |

22,63 |

21,64 |

45,15 |

2 375,49 |

2 464,9 |

|

2030 |

24,44 |

23,52 |

48,65 |

2 777,80 |

2 874,4 |

In Scenario 3 (pessimistic, 10% reduction), excise tax revenues on domestic goods in 2030 will amount to 788.70 billion soums for beer, 8.44 billion soums for wine, 2,489.23 billion soums for spirits (vodka), and 2,481.1 billion soums for cigarettes, for a total of 7,200.2 billion soums.

In this same scenario, excise tax revenues on imports in 2030 will amount to 24.44 billion soums for beer, 23.52 billion soums for wine, 48.65 billion soums for spirits (vodka), and 2,777.5 billion soums for cigarettes, for a total of 2,874.4 billion soums.

Figure 1. Excise revenue forecast with errors (up to 2030 for the studied ggoods studied

To empirically validate the projected increase in excise tax revenues from alcohol and tobacco products in Uzbekistan, we conducted multiple regression analyses using macroeconomic and policy-related explanatory variables over the 2016–2024 period. The dependent variable in the primary specification was total excise tax revenue, disaggregated data also allowed testing of domestic and import components.

The best-performing regression model, based on adjusted R² and theoretical plausibility, includes GDP (nominal), unrecorded consumption index, and excise tax rates on beer and vodka as predictors. This model explains nearly 99.8% of the variance in total excise revenue (Adjusted R² = 0.998), indicating a very strong fit.

Among the explanatory variables, the unrecorded consumption index emerged as a robust negative determinant, suggesting that improvements in enforcement and reductions in shadow market activity could directly increase official tax collections. The excise tax rate on vodka showed a consistent positive association with total revenue, aligning with Ramsey-type taxation theory, which supports targeting products with relatively inelastic demand. Additionally, population growth was found to be a statistically significant positive factor in alternative model specifications, reflecting the expanding consumer base for excisable goods.

Although GDP appeared as a negative coefficient in all models, this may be attributed to multicollinearity or shifting consumption patterns (e.g., toward informal channels) as incomes rise. Nevertheless, the combined empirical evidence supports the view that Uzbekistan’s excise tax revenues will continue to increase if current demographic trends persist, unrecorded consumption continues to decline, and excise tax rates are carefully calibrated, particularly on high-yield products like vodka.

These findings align with the theoretical justifications outlined earlier and provide a solid empirical foundation for the moderate and optimistic revenue projections presented in this study.

Conclusion

The forecast for excise tax revenues depends on changes in both internal and external factors that affect economic growth (such as world prices, the introduction of customs duties on imported products, the depreciation of the national currency, and changes in interest rates). In the optimistic scenario No. 2, excise tax revenues are expected to grow until 2030 years

However, the main function of excise tax is not only to form budget funds, but also to reduce the level of morbidity of the population, improve the state of atmospheric air, reduce inequality among citizens and expand access to quality public services. The approach and economic instruments we propose will help solve the above problems.

Considering that Uzbekistan is gradually moving to the WTO, the country must comply with the provisions of this international organization. Thus, excise tax rates on domestic and imported products, including natural gas, alcoholic beverages , must comply with international requirements. Since the excise tax rate on natural gas produced in the republic is 12% of its sales value, while imported gas is not subject to excise taxes. This violates the WTO requirements on the need to ensure equal taxation of manufactured and imported products[12].

It is also proposed to introduce a mechanism for tax offsetting of excise tax paid for enterprises that have a registration certificate or pay advance excise tax. In particular, when selling excisable goods, it is necessary to apply a system for offsetting excise tax paid on input materials and raw materials, including customer-supplied materials for which excise tax was paid by the owner earlier (for example, for business entities operating in the pharmaceutical sector).

In order to reduce the negative health consequences of people involved in gambling, as well as to increase budget revenues, we propose to introduce a tax on gambling (as is known, by the Decree of the President of Uzbekistan dated December 6, 2024, the organization of online games based on risk and bookmaking activities are officially permitted in the republic from January 1, 2025). The gambling business is a specific area of activity that has certain negative consequences for human health. In this regard, we consider it appropriate to introduce the corresponding tax from January 1, 2026.

Open Access By Aditum Open Access Journals id licensed under Creative Commons Attribution 4.0 International License. Based On a Work at aditum.org