Clinical Case Reports and Clinical Study

OPEN ACCESS | Volume 13 - Issue 1 - 2026

ISSN No: 2766-8614 | Journal DOI: 10.61148/2766-8614/JCCRCS

Nina K. Gogoll

Independent Author.

*Corresponding author: Nina K. Gogoll, Independent Author.

Received: May 13, 2026 | Accepted: May 19, 2026 | Published: May 22, 2026

Citation: Gogoll, N. K. (2026) “The Principal-Agent Relation as Part of the Corporate Governance” Clinical Case Reports and Clinical Study, 13(2); DOI: 10.61148/2766-8614/JCCRCS/241.

Copyright: © 2026 Nina K. Gogoll. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

Principal-agent relationship is part of corporate governance. In order to comprehend this relationship, this article critically and briefly discusses what is behind this relationship between the two parties. This article first explains principal-agent theory and then continues to present the management of incentives using the example of a value-oriented compensation system. Finally, the central findings are discussed and synthesized. The literature recommends agreements of incentives and adoption of systems of incentives to achieve long-term success and to navigate the interests of both parties. Indeed, a good example is a bonus bank with variation of direct payment as first and later payment, a so-called hybrid payment.

Methodologically, this article follows a formal-analytical research strategy that describes problem structures in a simple and largely abstract form. Therefore, principal-agent theory is presented first, and subsequently, a selected approach to incentive management based on a value-oriented system is introduced. This procedure is supplemented by a secondary analysis of relevant literature.

Principal-Agent Theory, Value-Orientated Incentives System, German Corporate Governance Code

1. Introduction

The German Corporate Governance Code contains of three central elements: firstly, it describes essential legal provisions concerning the management and supervision of publicly listed German corporations1, secondly, it formulates recommendations and suggestions are based on nationally, and thirdly, internationally recognized standards of good corporate governance. The Code aims to present the German Corporate Governance system in a transparent and comprehensible manner, and in doing so, it seeks to facilitate the assurance of international and national investors, customers, employees, and the public in the management and monitoring of publicly listed German corporations (compare (cp.) Regierungskommission Deutscher Corporate Governance Kodex, 2022). Furthermore, the following applies: “Corporate governance structures are supposed to reduce agency problems.” (Gogoll, 2023, p. 1159). This particularly concerns the so-called principal-agent relationship between investors and the top management of corporations.

To make the structure of this principal-agent relationship comprehensible, the present article first explains Principal-Agent Theory in subsequent section two, which examines the relationship between the principal and agent with its features of basic presupposition as well as illustrates the specific characteristics of information asymmetries between both parties. Section three, Managing Incentives in a Value-Oriented System, then introduces the management of incentives using the example of a value-oriented compensation system. In addition, it is merely proposed that the structure of incentive system be composed of various hierarchal levels and a bonus bank. Finally, the last section Discussion and Conclusion discusses and synthesizes the central findings.

Methodologically, the article follows a formal-analytical research strategy that describes problem structures in a simple and largely abstract form (cp. Grochla, 1978, p. 85). For this purpose, principal-agent theory is introduced first. Subsequently, a selected approach to incentive management based on a value-oriented system is presented. This procedure is supplemented by a secondary analysis of relevant literature.

2. Principal-Agent Theory

Principal-agent theory deals with analyzed service relationships as so-called client-contractor relationship (cp. Bernhold & Wiesweg, 2021, p. 117). Its objective is to design the contractual relationship between the principal (cp. Bernhold & Wiesweg, 2021, p. 117), that is, the owner or shareholder, and the agent, that is, the manager or responsible executive board (cp. Schömig, 2015, p. 12), as appropriately as possible.

In this context, the following basic presupposition must be considered:

- self-interest-maximizing behavior of the actors (cp. Lassar & Kerr, 1996, p. 14),

- existing conflicts of interests (cp. Rieg, Vanini, Gleissner, 2025, p. 27),

- bounded rationality of the actors (cp. Bernhold & Wiesweg, 2021, p. 117), and

- existing information asymmetries between principal and agent (cp. Brockmann, 2023, p. 149; Rieg et al., 2025, p. 27; Wirt, 2021, p. 61).

The last-mentioned aspect of information asymmetries in particular, gives the agent a specific discretionary and behavioral scope. The central problem areas of principal-agent theory contain Hidden Characteristics, Hidden Action, and Hidden Information (cp. Bantz, 2019, p. 24ff.; Ebers & Gotsch, 2019, p. 212f.; Rieg et al., 2025, p. 27; Wirt, 2021, p. 61), as well as the more demanding form of Hidden Intention (cp. Leider, 2019, p. 253) and Moral Hazard (cp. Brockmann, 2023, 149f.; Rieg et al., 2025, p. 27). These problem forms are explained in more detail below.

Hidden Characteristics refer to characteristics that already exist before contract conclusion (cp. Brockmann, 2023, p. 152; Ebers & Gotsch, 2019, p. 212f.; Spremann, 1987, p. 8). These characteristics impact the subsequent principal-agent relationship ex ante (cp. Bernhold & Wiesweg, 2021, p. 117f.). They are present in the agent but initially remain hidden from the principal (cp. Bernhold & Wiesweg, 2021, p. 118). This gives rise to the danger of adverse selection, whereby signaling, screening, and self-election are discussed as possible solution approaches (cp. Wirt, 2021, p. 60f.). Only after contract conclusion or after the service has been performed can the principal recognize the agent’s qualification (cp. Bernhold & Wiesweg, 2021, p. 118).

By contrast, Hidden Action and Hidden Information arise only after contract conclusion (cp. Bantz, 2019, p. 15ff.; Brockmann, 2023, p. 152 and p. 198; Wirt, 2021, p. 63). They refer ex post (cp. Cunningham, Menter & Wirsching, 2019, p. 554) to the agent’s activity (cp. Bernhold & Wiesweg, 2021, p. 118). In the case of Hidden Action, the principal cannot directly monitor the agent’s efforts and actions (cp. Bantz, 2019, p. 15ff.; Ebers & Gotsch, 2019, p. 213). If monitoring is possible, it often involves prohibitively high costs for the principal (cp. Bernhold & Wiesweg, 2021, p. 118; Paulitschek, 2009, p. 36, footnote 140). In the case of Hidden Information, the principal can observe the agent’s performance but cannot evaluate that performance professionally (cp. Picot, 1991, p. 152; Picot, Dietl, Franck, Fiedler & Royer, 2025, p. 110). In both cases, the principal knows the agent’s performance outcome but cannot clearly distinguish between external influencing factors that may have favored the result and the agent’s actual performance contribution (cp. Bernhold & Wiesweg, 2021, p. 118). Moral Hazard arises (cp. Wirt, 2021, p. 62) when the agent opportunistically exploits the described information asymmetry (cp. Shrestha, Tamošaitienė, Martek, Hosseini & Edwards, 2019, p. 6458). The risk increases with the agent’s behavioral or control scope (cp. Picot et al., 2025, p. 110; Schömig, 2015, p. 13, footnote 57).

The problem of Hidden Intention describes the circumstance that the agent’s intentions become visible to the principal only after contract conclusion (cp. Ebers & Gotsch, 2019, p. 213). The principal then recognizes the agent’s opportunistic behavior but has only limited or no possibilities to effectively counteract this behavior and induce the agent to change it (cp. Bernhold & Wiesweg, 2021, p. 118). The more pronounced the dependency relationship between principal and agent is, the greater the risk of Hidden Intention for the principal becomes and consequently, this can result in a hold-up problem (cp. Brockmann, 2023, p. 151f.; Ebers & Gotsch, 2019, p. 213).

Precisely these last basic presuppositions provide the actors with a scope of action that they can use to increase their own utility or maximize their own compensation (cp. Bernhold & Wiesweg, 2021, p. 117). Therefore, the principal attempts to influence the agent’s behavior (cp. Wirt, 2021, p. 60) through suitable agreements of incentives or systems of incentives (cp. Bernhold & Wiesweg, 2021, p. 117). For this reason, the following third section outlines the example of a value-oriented pay-for-performance system.

3. Managing Incentives in a Value-Oriented System

Suitable agreements of incentives or systems of incentives are generally agreed upon between the parties involved in order to align their interests, these include, for example, financial bonuses, contractual penalties, or other forms performance-based compensation (cp. Leider, 2019, p. 253). In addition, such systems can contribute to satisfying information needs within the framework of general financial reporting.

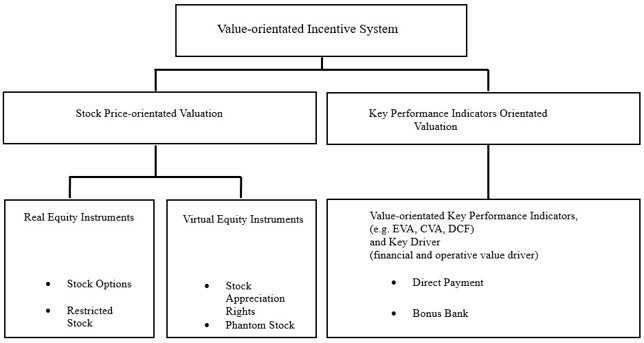

There is a variety of different pay-for-performance systems, as Pellens (cp. 1998), among others, already showed in 1998. Pellens, Crasselt and Rockholtz (cp. 1998, p. 12) present an overview of value-oriented incentives system, which is described in more detail in the following (cp. Weber, Bramsemann, Heineke & Hirsch, 2017, p. 166):

This overview comprises, on the one hand, a stock-price-oriented measurement basis with real equity instruments such as stock options and restricted stocks as well as virtual equity instruments such as stock appreciation rights and phantom stocks. On the other hand, it comprises a key-performances-indicator-oriented measurement basis with various value-oriented key performances indicators, such as Economic Value Added (EVA), Cash Value Added (CVA) or Discounted Cash Flow (DCF) (cp. Brühl, 2025, p. 503ff.; Steiner & Landes, 2017, p. 192ff.). These indicators can lead either to a direct payment or to a bonus bank or incentive bank. Figure 1 presents this value-oriented incentives system described above2.

A value-oriented incentive system can generally be designed using the same elements and contexts that also apply to other incentive systems, where different hierarchical levels require different measurement bases as well as different proportions of variable and fixed compensation components, and in addition, the influence of the capital market must also be considered at each level of the incentive system (cp. Weber et al., 2017, p. 157)3.

Weber et al. refer to a variant of payout through a bonus bank, in which bonus payments are accumulated over several years and, if necessary, offset against potential penalty payments in later years (cp. Weber et al., 2017, p. 169)4. After a vesting period, the accumulated amounts are paid out either as a cash payment in the form of taxable compensation or, alternatively, granted in shares or stock options (cp. Weber et al., 2017, p. 169). The latter has the advantage that short-term-oriented behavior by the agent can be sanctioned in later periods, so as a result, the agent is encouraged to engage in long-term planning and long-term-oriented behavior (cp. Weber et al., 2017, p. 169). This behavior more closely corresponds to the interest of the principal or the corporation. Brühl (cp. 2025, p. 511ff.) promotes to deposit the earned bonus in a bonus bank, that possible penalty payments are offset against the deposit, and that a certain agreed percentage of the earned bonus is paid out annually, for example 40%. From the agent’s perspective the date of outpayment is relevant, which depends on the height of percentage rate, however, the height is a corporation-political decision and therewith, the nature of the outpayment is accompanied by either a short-term or long-term trend (cp. Brühl, 2025, p. 512).

The following final section discusses and synthesizes the findings obtained.

Figure 1: Value-oriented Incentives System

Source: Author’s own in accordance with Pellens et al., 1998, p. 12; Weber et al., 2017, p. 166.

4. Discussion and Conclusion

Corporate governance forms the framework for regulated interaction among all significant stakeholder groups with particular focus on the relationship between owners and corporate management, whereby responsible corporate management and corporate monitoring are intended to reduce the principal-agent conflict as far as possible, and at the same time, the interests of groups requiring protection, such as minority shareholders, should be taken into account, and a sustainable as well as long-term value orientation should be pursued (cp. Mondello, 2022, p. 48). The explanatory statement of the German Corporate Governance Code makes clear that corporate governance cannot be based exclusively on the principal-agent model (cp. Regierungskommission Deutscher Corporate Governance Kodex, 2023, p. 1, II. No. 4). Nevertheless, the actors involved must consider the principal-agent relationship, since its occurrence cannot be disregarded.

Principal-agent theory illustrates the structural problems between principal and agent. The literature shows that self-interest-maximizing behavior, conflicts of interest, bounded rationality, and information asymmetries between principal and agent, in particular, must be considered in a contractual relationship. Information asymmetries provide the agent with scopes of action that may be associated with Hidden Characteristics, Hidden Action, Hidden Information, Hidden Intention, and Moral Hazard. This creates a need for preventive control measures on the part of the principal.

The principal can influence the agent’s behavior through suitable incentive agreements or incentive systems. In this way, the agent’s behavior is intended to be aligned more closely with the interests of the principal or the corporation. One possibility for managing these incentives is the value-oriented incentive system presented above. This system allows the incentive agreement to be based either on a stock-price-oriented measurement basis or on a key-performances-indicator-oriented measurement basis. In addition to incentive agreements or incentive systems, the literature proposes a bonus bank. In this model, bonus payments are accumulated and offset against possible penalty payments in later years. This design promotes long-term planning and long-term-oriented behavior by the agent. Moreover to a cash payout as taxable compensation, payment in form of shares or stock options is also possible. Furthermore, it appears useful to define a performance indicator whose achievement or improvement serves the utility of shareholders and, at the same time, functions as the measurement basis for variable compensation components (cp. Schömig, 2015, p. 16).

From the principal’s perspective, a value-oriented incentive system is suitable for guiding the agent’s behavior. A delayed payout through a bonus bank also appears appropriate, provided that no penalty payments arise in later years. However, the fact that a waiting period of several years for already earned incentives may weaken the motivational effect of the system must be considered. For this reason, a hybrid design, as shown by Brühl, is advisable, combining direct payments with later payments tied to long-term goal achievement.

1 Those are primarily governed by the German Stock Corporation Act (cp. Regierungskommission Deutscher Corporate Governance Kodex, 2022).

2 See for further readings Pellens et al., 1998, p. 11ff.; Steiner & Landes, 2017, p. 187ff.; Weber et al., 2017, p. 163ff..

3 Another example is a non-value-oriented incentive system that shows the basic structure of a performance-based incentive system which consist of the components base compensation, performance-based bonus as well as corporation-based bonus, whereof each component is weighted with different percentages. These percentages can vary significantly, for example, higher variable compensation is standard in top management and sales. Also, different kinds of incentive systems between fix-based compensation orientation and performance-based orientation are illustrated in comparison, cp. Steiner & Landes, 2017, p. 55f. and illustration 24.

4 This is similarly stated by Steiner and Landes (cp. Steiner & Landes, 2017, p. 64ff.) as well.

Open Access By Aditum Open Access Journals id licensed under Creative Commons Attribution 4.0 International License. Based On a Work at aditum.org